There are many ways to write “state of industry” posts. One approach is to project the future based on trends established this year. Another is to project the future based on the current strategies employed by the top industry players.. I did some version of that in 2014 and 2015. This year, I thought I’d focus on a different approach – go back to first principles and look at business models.

This approach will help us pivot from the industry’s perspective to the customer’s perspective and, thus, not be too focused on technology fads (e.g. Segway, Google Glass, etc.)

We’ll approach this in 3 parts –

I. The 4 core business models

II. 2016 – what we saw

III. 2017 and beyond – what we might see

Couple of notes of caution

- This is an attempt to focus on things that are likely to matter most in my personal opinion. It’s not an exhaustive list. I’ve pointed to 10 posts at the end which, together, should add more context and analysis.

- I’ve spent a lot of time on context/foundation given how important it is to power meaningful discussion.

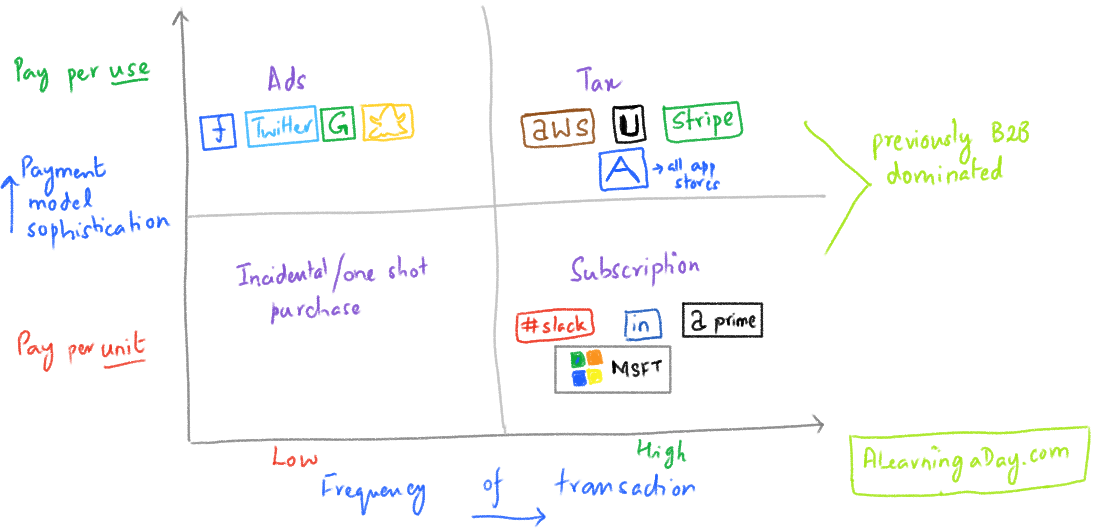

I. The framework:

I contend that there are four fundamental business models on the internet and, since we’re talking about money, lay them out in two axes – frequency of transaction (a proxy for customer loyalty) and payment model sophistication (pay per use is much more sophisticated than pay per unit). There are many, many customer acquisition models (e.g. freemium). However, all these models bring us back to these 4.

- One-shot purchases: This model is used by anyone who can or has sold stuff online. Thanks to the internet, we can go into business on the internet and sell anything to, pretty much, anyone.

- Subscriptions: Or something-as-a-service. Thanks to the flexibility and collaboration cloud based services provide, the internet has enabled more subscription businesses than ever before. In essence, it hasn’t “created” subscription businesses as often as converting previous “one shot purchases” to subscription businesses (think: Adobe’s conversion to Photoshop-as-a-service and Microsoft’s ongoing conversion to Office-as-a-service). Subscriptions used to exist before but the internet has turbo boosted them.

- Ads: Ads have always been a constant 1% of the GDP long before the internet. Ad money just goes where consumer attention goes. However, there was an old world marketing managers quote – “Half of our advertising budget is wasted. The problem is we don’t know which.” While this hasn’t been fully solved by the internet, the amount of data available means digital marketing measurement system is light years ahead of old world systems. Now, advertisers can pay per click or even per conversion.Typically ad businesses jump into this matrix from outside of it altogether. You rarely see a business based on “one stop shopping” become an ad business. Instead, we see social/consumer networks that focus on user growth (and no revenue) that hit critical mass that then morph into ad machines (think: Facebook, YouTube, Snapchat).And, ads are low on customer loyalty because advertisers aren’t loyal to the platform. They’ll go wherever customers spend time.

- Tax: The tax model focuses on earning money when your customer earns money. It is powerful because it is aligned to a customer’s revenue growth versus a growth in headcount (as in the case of most B2B subscription services). On the internet, tax is typically how platforms (think: App stores, AWS, Uber, AirBnB, PayPal, Kickstarter) make money. Everybody wants to become a platform because the tax model is very lucrative. But, it is also very hard to get critical mass as a tax based business and typically take vast amounts of funding, grit and luck.

An important note – these models are not unique to the internet. The old world had examples of each of these models. For example –

- One-shot purchases (massive scale): Traditional retail

- Ads: Traditional newspapers

- Subscriptions: Traditional newspapers or cable

- Tax: Book or game publishing

However, the internet changes the nature and scale of these models. And, in doing that, it completely disrupts existing businesses.

Disruption. Every conversation about disruption calls for the customary nod to Prof Clay Christensen. Over the years, Prof Christensen replaced the term disruptive technology with disruptive innovation because he recognized that few technologies are intrinsically disruptive or sustaining in character; rather, it is the business model that the technology enables that creates the disruptive impact. Disruptive technologies, thus, are often novel combinations of existing off-the-shelf components.

Just to make that point, let’s consider one industry that is currently being disrupted – retail.

Traditional retail was built on assumptions of scarcity. The main business model was “one shot purchases” –

- You walked into the retail outlet, bought something and walked out.

- Retailers strived for transactional loyalty, of course. So, retailer loyalty cards were important. Once you committed to a Sam’s Club membership, you were likely to make more of your purchases at WalMart. And, that mattered. However, proximity to your home mattered a LOT more.

- Retailers had limited shelf space. So, they typically had a few large companies across various categories that fought hard for that shelf space. These companies – P&G, Unilever, Kraft, Black & Decker, etc. – were very profitable. They, then, used these profits primarily to sponsor advertising which ensured customer demand and, then, guaranteed distribution at retail outlets all over.

- They guaranteed distribution at retail outlets by a series of extensive discount and rebate schemes (i.e. a channel strategy) that enabled them to pass some of those big profits to their important retailers.

- While these companies dictated terms with most retailers, important retailers like Wal Mart had the upper hand. In a world of scarcity, aisles at Wal Mart were scarce and critical to success.

- So, even if Iam’s had the best pet food product on the market, they needed access to that limited shelf space to reach the mass market. So, being acquired by P&G made a lot of sense.

Isn’t it amazing how a discussion on traditional retail touches all industries that sold product (i.e. all consumer packaged goods) and traditional advertising?

On the internet, retail is built on the assumptions of abundance. The dominant business models are subscriptions and tax.

- You have access to anything, anywhere. You could, literally, find the same item on many websites. In many cases, you could actually just by-pass the online retailer and buy straight from the creator.

- So, the value of the retailer now lies in your loyalty. If you are subscribed to Amazon Prime, you will perform your product search on Amazon, and not Google. That is the difference between success and failure on the internet. (Side note: In such a noisy world, branding matters a lot. Hence, the success of the likes of Apple and, so far, Tesla)

- Subscriptions are not the only way to build a retail business, of course. There are multiple platforms that make money via the “tax” model. Etsy, eBay, and even Amazon, enable third party sellers to sell their wares.

- But, if you are a small business looking to sell on the internet, you can now leverage the power of subscriptions to sell to your customers. And, Dollar Shave Club, Birchbox, et al, have led the way in doing that. In a world of abundance, subscriptions is how modern retailers ensure your loyalty.

- Of course, selling music or razors or books on the internet is different from selling on the cloud. You don’t have to worry about all the crazy distribution costs. Everything can be much cheaper.

Retail is still in the early stages of being disrupted. But, as Benedict Evans points out, it is only a matter of time. And, while retail is fundamentally about a customer buying something, the way it happens determines the economics of the whole process. And, the internet has changed how buying happens. Stay tuned.

II. Reflect on what we’ve been seeing up in 2016

One shot purchases. Of the 4 internet business models, one shot purchases makes less waves because it is, by far, the least sought after model. This is the piece of the internet reserved for the small businesses who can just create their own little online store with tools from the likes of a Magento or Shopify. The goal, here, is to build a brand and figure out a way to build a subscription.

There’s too much going on to trust that a customer will come back to you.

Subscriptions. Subscriptions, once again, had a big year. Let’s go through a few of the big moves.

- LinkedIn was acquired by Microsoft in the biggest acquisition in tech history. A big move for Software-as-a-service. ~70+% of LinkedIn’s revenue is subscriptions.

- The competition for B2B messaging-as-a-service intensified. Microsoft and Facebook took on Slack and HipChat for the B2B messaging-as-a-service market. This is important because the eventual winner of this race could create a platform for Bots and make money as a “tax” off its bots – à la app store.

- Apple signalled its attempt to commit heavily to subscriptions (“services” in their words – i.e. AppleCare, iCloud). This is another demonstration of the might of subscriptions on the internet. This isn’t Apple’s first experience with the idea of subscriptions. It is easy to forget but it sells many iPhones effectively as subscriptions. Pay every month for 2 years. Then, upgrade to the next phone. Many Apple loyalists are perennial product subscribers. The difference, this time, is that subscriptions on the cloud require a very different “ship fast, iterate quickly” culture as opposed to pseudo-subscriptions in a product based world which are based on “ship once, get it absolutely right and maintain the customer connection via financing.”

- The App store enabled app developers to charge via subscriptions. About time. There’s still a lot of work ahead for the app store to make this process easier. But, this was a start.

- Soap-as-a-service. The launch of Amazon Dash buttons beautifully illustrates why the tax and subscription models are the place to be. P&G would like you to get the “Tide” Amazon dash button so you don’t ever do a search for a competing product. And, Amazon loves it because they charge P&G a tax for every Tide satchel stored.

- SaaS investments (mostly B2B) are going very strong. Crunchbase data shows that global SaaS funding has gone from $1.5B in 2010 to $7B in 2015.

- Hundreds of start-ups are building interesting, viable B2C subscription businesses – something-in-a-box. Just check this list of 70+ start-ups that all sell something-in-a-box. Wines, food, fashion – you name it and it is there.

Ads.

- Facebook and Google continued to grow at ridiculous rates. Facebook and Google have been taking in most of the ad growth and conquering the very lucrative mobile display ads and search ads respectively.

- Facebook had all sorts of measurement issues. This led to a call for better 3rd party verification of metrics. Or, maybe another ads behemoth that can challenge Facebook to keep them honest.

- Snapchat grew in momentum. Snapchat is on its way to a reported $30B+ IPO. They followed the playbook to build a social network based on ads – start with a risque use case for a small core of users, keep innovating to meet the needs of a larger group, make fun of ads, refuse to monetize, continue growing. And, finally, when they hit critical mass, run ads anyway. To their credit, Snapchat have done well with different ad formats. But, at the end of the day, ad businesses are about attention. And, Snapchat has a better grasp on millenials’ attention in the US than almost all other businesses (Instagram is probably the only other real competitor)

- Non social media publishers were frustrated at only seeing a small percentage of ads revenue. A lot of the money in the ad space is in the “tax” business model – all of ad tech is effectively a tax. All this results in large publishers growing frustrated about only seeing a small percentage of ads revenue on their site.

- Internet TV took on real TV. Netflix and Amazon Prime Video are among the top 6 global content creators. YouTube, Facebook and Snapchat video all went after TV budgets as part of the ever expanding digital pie. The more people transfer their TV viewing time to the internet, the quicker this shift will happen.

Tax.

- Everybody who wants to be a platform should learn from Amazon. They continue to show us how the tax model is done. AWS, Amazon Fulfilment service, Kindle are all great examples of this business model. There are many ways Amazon could do more of this – could there be a delivery-by-Amazon tax service (feat: drones) coming in the future? And, Alexa is clearly headed to be a platform tax in our homes.

- Stripe becoming a powerful tax business. All of payments is built on the tax business model. So, Stripe’s growth as a payment provider is significant this year (worth $9B now). Stripe added an innovative customer acquisition model with “Stripe Atlas.” For a fee, Stripe will help you incorporate your company in the US (all of us can be global one-shot purchase or subscription retailers, of course). And, of course, Stripe will automatically become the payment tax for your business. Brilliant.

- The race to become the platform of everything transportation related intensified. Uber pulled out of China. Lots of investment in Asia with companies like Didi, Ola and Grab. The action will continue.

- AirBnB had a challenging year – even with tremendous growth. AirBnB moved traditional hotel stays (largely one shot purchases) into a tax model – similar to Uber. And, similar to Uber, they’re trying to do a lot more than what they started with – flight bookings, travel planning, etc. However, there’s a lot of regulation against being the one global platform for rooms. And, AirBnB has been fighting that. Then, of course, there are all the issues with discrimination on the platform.

- Lots of consolidation in ad tech led by Adobe and Salesforce. Ad tech, as mentioned above, is a classic example of tax revenue. There was a ton of consolidation in the ad tech world as Adobe and Salesforce acquired companies to be an advertisers one-stop “data management platform.”

- Slack and Facebook trying to be tax platforms a la WeChat. Their play – bots.

III. Explore what we might see in 2017 and beyond – with a lens on the trends everyone talks about.

I am no prediction expert. But, I thought we’d touch on 4 interesting emerging technologies and what I think their dominant business models would be.

Artificial intelligence. I think AI having 2 kinds of implementations –

- For existing businesses, I think of Artificial Intelligence as a loyalty creator. I think deep learning will help existing technology giants deeper their connection with customers. It is hard not to bet on the giants (e.g. Amazon, Microsoft and Google) thanks to the massive amounts of data that powers their efforts. This is happening already.

- But, that said, I also expect many entrepreneurs leverage open source libraries like TensorFlow to create interesting implementations in niche fields (examples here) that the big companies won’t bother going after. We should either see some very high value start ups acquired by the giants and a potential giant-of-the-future emerge by building an extremely sticky product for a small niche and, then, gradually expanding. And, I expect these to be subscription businesses. I think it is unlikely we’re going to see a tax based platform given the giants’ moves to open source AI.

Related note on self driving cars – could the future of cars be a shift from one shot purchases to subscriptions? Since disruption lies in business models, subscriptions may be the future of car ownership. In a world with rented self driving cars, maybe we’re looking at a future where we pay company X a fixed amount for unlimited use in the year?

Augmented reality/Virtual reality. There are lots of options in play here. Snapchat has taken a stab at augmented reality through their glasses. That suggests AR/VR could be an interesting play for consumer attention and, potentially, monetization via ads. This isn’t hard to imagine – you are in your virtual Facebook/Pokemon Go world and there are billboards everywhere with ads for you to look at.

However, I think there’s potentially a few subscription businesses in AR/VR. Think: $1000 a year for travel subscriptions (spend time in your dream locations) or $500 a year for gaming tournaments (play X virtual games with your global team).

Finally, we could envision “tax” based monetization as well. An AR/VR company could help you buy clothes that fit a virtual you and charge retailers per use (perhaps a more advanced version of LikeaGlove?).

The Internet of Things. I think a successful implementation of internet-of-things is going to result in 2-3 massive platforms who make their money as a tax. We need the equivalent of the iPhone and Android ecosystems for our toasters. The road to that sort of standardization isn’t really clear. But, if and when that happens, I think tax will be the way to go. And, if I had to bet on a company to do this, I’d bet on Amazon. What if private label Amazon toasters could connect to the internet and be controlled by Alexa?

Related and very interesting, what if an embedded chip in your Tide packet could send a signal to your Amazon Dash button to put a Tide refill packet in your cart?

Bitcoin and Blockchain. Bitcoin has had its best year yet. I think Bitcoin, a digital currency with near zero transaction costs, will make the implementation of “pay-per-use” even more prevalent. But, it will also accelerate the – everyone is a retailer on the internet phenomenon. One reason that shift isn’t happening fast enough now is because of cross-border currency restrictions. Just imagine what happens when all those something-in-a-box subscription businesses have easy access to a global market. Another example – if micro-payments become real easy, could we pay per article read? Then again, if this cross border stuff happens, there will likely be new regulation hurdles.

The underlying Blockchain technology commoditizes trust and identity. I don’t understand the full implications of what online communities built on Bitcoin would be. But, as it is decentralized technology, a blockchain based Facebook will likely not see ad profits accrue to a comparatively tiny group of folk as they do today. Potentially very disruptive. But, my sense is that we’re still 4-5 years from seeing this playout. Also, blockchain tokens are a very interesting implementation of the tax model.

Conclusion: There is a lot going on in tech and it is hard to really understand going on by following the news. A simpler, and yet effective, approach is to create mental models that help us make sense of all of this. One such approach is to look at the core 4 business models. At the end of the day, every promising technology has to prove its worth to survive. And, thinking about how emerging technology could change existing business models can be a powerful way to think about the future. At any rate, that’s how disruption is done.

10 interesting posts in case you want to dig deeper.

- Disruptive innovation: Disruptive Innovation by Wikipedia

- Internet scale: Mobile is eating the world by Benedict Evans

- Infinite Shelf space: Dollar Shave Club and the disruption of everything by Ben Thompson, Stratechery.com

- Tesla’s brand: It’s a Tesla by Ben Thompson, Stratechery.com

- Disruption in publishing: Publishers and the smiling curve by Ben Thompson

- SaaS funding: Just How Global Is The SaaS Startup Phenomenon? By Tom Tunguz

- Google and Facebook’s ad growth: Google, Facebook Leave Rivals Struggling for Digital ‘Nirvana’ by Melissa Mittelman and Alex Sherman, Bloomberg

- Snapchat’s impressive growth: While We Weren’t Looking, Snapchat Revolutionized Social Networks by Farhad Manjoo, NYT

- Amazon’s tax success: The Amazon Tax by Ben Thompson, Stratechery.com

- Bitcoin’s best year: The underpinnings of bitcoin’s bull run look way more solid this time by Joon Ian Wong, Quartz

(Thanks EB, Kaushik, and Pranav for all the edits on this – and to all other friends who helped with the thinking)