Last year, as I was preparing for interviews, I spent a few days going through all posts from my favorite technology analysts – Ben Evans and Ben Thompson – and put together a synthesis of everything that happened in tech in 2014. It was a fantastic exercise as it both taught me a lot and helped me a great deal in my interviews.

As I was recommending this strategy to anyone who would listen, I realized that I should continue doing this once every year as an investment to the wonderful industry I’ve chosen. I was inspired by Bill Gates’ think-week in doing so and realized that it would help me actually “study” and internalize what I’d read about via blog posts and emails in 2015. So, voilà – here’s my synthesis of Tech in 2015. The raw material that helped form this post is primarily covered in two posts from the 2 Bens – 16 mobile theses by Ben Evans and The Stratechery 2015 in Review by Ben Thompson. Big thanks to blogs from Albert Wenger, Fred Wilson, and Tom Tunguz, as they’ve all informed my point of view through the year.

Fair warning – this is a monster post and will be a long read. 80% of the content of the post is thanks to the 2 Bens. However, there’s probably a good bit of thinking that’s just me. I’ve tried to call it out. Either way, just wanted to warn you. :-) To make things easy, I have avoided hyperlinking to a 100 other places. That aside, I hope it will be worth it.

Tech in 2015 – what we saw.

I’ve broken this part down to 3 pieces –

I. The cloud

II. Mobile

III. User experience – user experience is the largest chunk of this post simply because it helps us get to a whole host of topics

1. The cloud saw a fascinating year with AWS’ break out success.

Amazon.

Breaking out AWS numbers in their financial filings was significant for Amazon – it made public what many suspected, that AWS was a fast growth and high profit (by Amazon standards at least) business. The genius of AWS has been written so many times that I don’t planto delve into details into how it works. Suffice to say that nearly ever emerging startup uses AWS and grows with AWS. Amazon has benefited so much from economies of scale that companies like Netflix and Dropbox have continued to simply use AWS versus build their own data centers. Additionally, in a game where pricing matters a lot, Amazon not only has the lead but the culture to fight off its main competitors, Microsoft and Google, who are used to much bigger margins. Incentives matter.

AWS’ success was probably the largest driver in the Dell-EMC merger. After years of ignoring the trend toward storing data in the cloud, it’ll be interesting to see if Dell and EMC manage to keep their customers from switching to cloud storage. Large enterprises are understandably nervous of moving their data to the cloud. The big question is – will that change? Dell-EMC is likely betting (or hoping?) that it will not.

In Amazon’s case, AWS’ success matters a lot because Bezos has relied on cash rich businesses (primarily media sales in the past) to fund other experiments. And, AWS promises to be Amazon’s cash cow for the next decade.

Even if we’re not exactly on topic, I want to take a moment to also highlight the thread that ties their retail experiments together. This was the year of Amazon doubling down on an omni-channel strategy. I have written about this in detail – but, to cut a long story short, retailers typically become successful by excelling in one channel, e.g. brick and mortar or online. But, as they grow and take on more products (this applies less to a one-category retailer like Blue Nile), it makes business sense to develop other retail channels. This is because fast moving goods are suited to the brick-and-mortar channel while goods with massive selections/long tails (e.g. books and CDs) are more suited to an online channel. An omni-channel approach enables Amazon to maximize supply chain profits for each product category. As Amazon creates more physical locations for its highest demand product (this is inevitable), we will expect to see larger margins in its retail business. This is exactly what should send chills down the spine of any prospective retail competitor. As Amazon has continued to experiment and invest for growth, it is creating a massive moat that will make it very hard for anyone to compete directly.

Back to AWS for a moment, an industry that has felt AWS’ impact has been venture capital. Thanks to AWS greatly reducing the costs of starting up, it has resulted in a proliferation of Angel investors in the market. These angels have chosen to invest their millions in promising start-ups and VC’s have been forced to move up the chain and deal with larger funding rounds. They have been squeezed from the top end by massive funds such as Tiger Global that invest in portfolios of unicorns. VC’s used to run the table from Series A to D. Now, thanks to Angels, the old Series A has become an Angel round and so on. Interesting times.

A quick note on the Amazon New York Times saga.

The New York Times published a sensationalist article on Amazon’s brutal culture. I thought the piece was very one sided. A large proportion of the white collar workers at Amazon have their pick of options. However, I believe many of them choose to work at Amazon because they either clearly love the impact their work has on the world or because they believe it is good for their careers. Some of the world’s most influential organizations have had tough cultures that flow from their leaders. Not everyone would love to work for a tough leader like Jeff Bezos or Steve Jobs but there are enough who do. It may not work for everyone and that’s okay. As long as it works for a sizeable section of the population, it is hard to argue about their impact on our lives. I also think it is easy to moralize about culture by comparing every company to Google. It is easy to forget that Google’s culture was a result of its technical superiority and success and not vice versa. It is hard to create a cost conscious retailer (that’s how Amazon began) without a tough, margins focused culture – just ask Sam Walton. And, credit to Amazon, they’ve done that successfully and then done a whole lot more.

Microsoft, on the other hand, struggled with the cloud in the past decade because their incentives were all based on success on the desktop. These inevitably meant resisting mobile. And, the cloud and mobile (more below) go together. Satya Nadella has changed that with a massive focus on mobile with Azure and excellent mobile products and acquisitions (E.g. Accompli) followed by partnerships with storage competitors like Box and Dropbox. It isn’t easy to transform a massive, successful company – so great to see the much needed change of focus in Redmond. A lot of Microsoft’s struggle can be attributed to the struggle between a horizontal model vs. a vertical model.

Horizontal models vs. vertical models.

We tend to regularly see a tension between horizontal business models and vertical business models. An example of these is the tension between being an advertising companies (horizontal) and a platform (vertical). Advertising, for example, works well for B2C businesses (e.g. Facebook). Windows, on the other hand, was the dominant platform of the PC era – a platform becomes a platform when all the players earn more from being on the platform than the platform creator itself. It requires a continuous investment in the ecosystem. And, it is impossible to do well as a platform if you are optimizing for your own ad views. This is a tension we see most big companies face – Amazon faced it with the Fire phone (they aren’t suited to a vertical model as their performance should be good on every device), Google faces it every day (more later) and so does Microsoft. Additionally, while consumers who access products for free may be tolerant for ads, enterprise businesses do not. As a result, Satya Nadella’s push has been for Microsoft to de-prioritize the vertical Windows based model and focus on getting their products (e.g. Office) across all devices. Not easy.

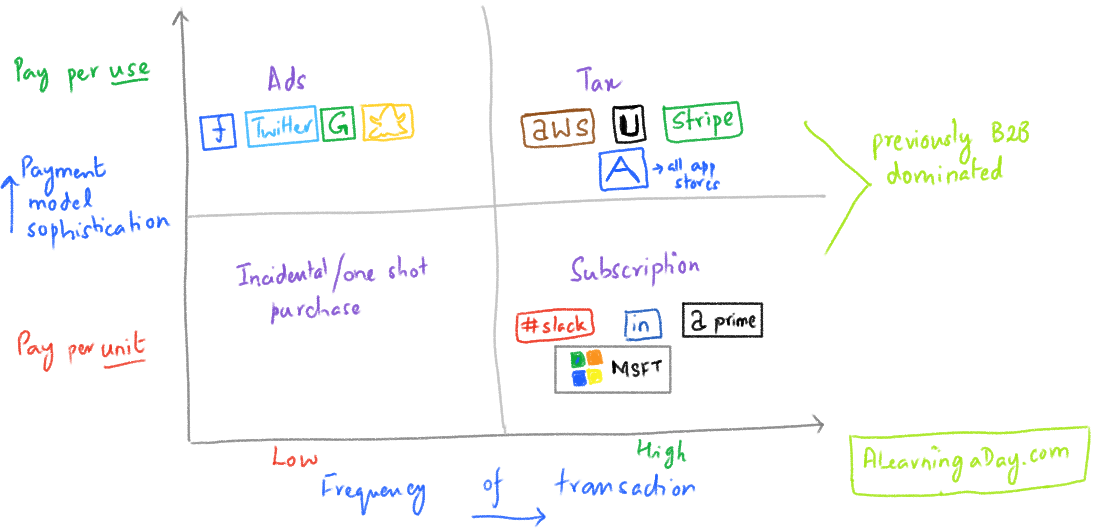

Shifting to B2B and B2C2B businesses on the cloud – now that we’ve established ads don’t work, subscriptions become the dominant business model. Adobe caught on to this early and switched its products to subscription products. I’d wager that Adobe is probably the company that has most successfully navigated the shift to the cloud. Subscription products are excellent businesses because of the recurring revenue stream (hence, more investment in Saas/software-as-a-service businesses). This allow companies to iterate constantly and keep improving their products while building long term customer loyalty. Box caught on to this early and pivoted from a customer focused product to an enterprise focused product. Dropbox, on the other hand, took much longer. Even if Dropbox scores on user experience (I am a fan so I am biased here), they have their task cut out if they hope to better Box’s success.

II. Mobile – the smartphone is the sun.

I don’t think it is possible to have a discussion around mobile in tech without a Benedict Evans graph. :-) So, here goes

The scale of smartphones is at a scale never seen before. Somewhere between 3.5 billion – 4.5 billion out of the 5 billion or adults own smartphones and upgrade every 2 years. It dwarfs the PC industry. And, as a bonus, we also take it everywhere. So, everything is being built or rebuilt for smartphone use. Here, Ben Evans’ analogy of the smartphone being the sun is spot on. There is a whole solar system being worked on around the smartphone (wearables, internet of things, TV etc.). But, it is clear that, at least for the foreseeable future, the smartphone will be at the center of things. Thus, mobile isn’t part of the internet, it IS the internet. Talk about mobile use cases and a mobile strategy is a sign that you’ve completely missed the boat. It is the desktop that is limited – you need to fire up a browser to access the internet on a PC. On the phone, switch on your Wifi and the internet talks to you via notifications.

But, what is mobile? Does it just mean a device with a small screen? Ben Evans believes it has 4 components –

- Operating systems that are easier to use. iOS and android vs. windows

- Better security. No infected floppy drive sort of worries

- More efficient chips. The energy efficient ARM ecosystem vs. Intel

- Scale. Mobile’s scale is 10x that of Wintel.

So, mobile is less about the device and more about an ecosystem that works very well together. So, in the next decade at least, we will definitely have a “mobile device” – likely small screen – and maybe, a larger screen device that is close to the old world “PC” – run on a Wintel or Mac ecosystem. Hence, mobile = sun. It’s been 9 years since the launch of the iPhone and the platform wars are done – Apple and Google have both won. iOS has taken over the more lucrative high end while Android has taken over the low end. Let’s discuss both.

Apple.

This is what Apple is betting on with the iPhone. The iPhone will be the center of your life with Homekit (internet of things), Carplay (cars), Healthkit (wellness), etc.

How successful is the iPhone going to be?

I think it is inevitable that growth will slow down. They have already captured a major chunk of the market that can afford it. Where the disruption theorists went wrong is that this chunk of the market is massive. Additionally, 2 year replacement cycle means this can be a source of continued profits as long as the iPhone maintains its edge with a super user experience.

Getting to the watch.

Computers have moved to smaller and smaller devices – mainframes, desktops, laptops, and now phones. The smaller they became, the more portable they became. The question, then, is where will this trend stop? Will it stop with the phone or will we end up at a smaller place – the watch?

So, the Apple Watch.

Apple’s strategy becomes very important here. By investing in the watch, Apple has, in effect, hedged against the possible demise of the phone. I suspect the Watch is an experiment of sorts of how mainstream a wearable can be. It matters that Apple was the company that released a watch. No other company commands loyalty the way Apple does and this loyalty is critical in people tolerating the issues with a version 1 of the watch. It doesn’t look like v1 of the watch succeeded. User reports frequently indicate that users stopped using the watch a few weeks in.

However, I expect investment in the Watch to remain a strategic priority for Apple because of a number of reasons – performance of future editions of the watch will improve, developers will build apps that suit the watch, Siri will get better with most people using it and, most importantly, it will mean Apple has a place in people’s wrists. If the wrist replaces the pocket as the location of the “new sun,” then Apple will want in.

All of this still assumes the watch is a technology product. What if we looked at it as a luxury product instead? Does it matter if it doesn’t work as well as long as it looks good? Doesn’t it further improve Apple’s brand and luxury/”aspirational” positioning? To be determined.

Fitbit.

Fred Wilson’s excellent end of year post suggested that he is long on Fitbit’s prospects. I use a Fitbit and love it. I am, however, skeptical about its future. I see 2 issues – I believe its narrow focus on health tracking (of which it really only does steps really well ) will not be enough to sustain user loyalty. It faces competitors from two ends – on the top end, you have the Apple watch that can do all it does. At the bottom end, you have competitors like Xiaomi whose bands last 45 days without needing a recharge for 15-20% of its price. Fitbit’s user experience may be better than Xiaomi for now. But, not by much.

Additionally, and this is entirely anecdotal, my list of inactive friends on Fitbit is much much longer than my list of active friends. It points to a retention problem that feels natural for a single purpose product.

(Fred, interestingly, predicts a different kind of wearable – perhaps something that could be worn on the ear. I still think we haven’t seen the end of the watch use case. As Fitbit demonstrates, there’s something about the wrist….)

A pit stop at Internet of things.

Discussions on wearables naturally lead to discussions on the internet of things where we will have more devices and things we use connected to the internet. While there are many companies doubling down on investments on this (Samsung, Xiaomi, Cisco et al), I suspect it’ll come down to how Google and Apple decide to push this forward. I say this because all these things that get connected to the internet will still be connected to your smartphone. And, Google and Apple control that part of the experience.

A case could be made for Xiaomi which offers a modified Android experience. I don’t know enough about Xiaomi so I find it hard to comment. The only reason I’m skeptical is because Xiaomi, to me, targets the higher end Android user (of which there are many for sure). And, these users seem to be switching to iPhones the moment they can afford an iPhone.

Apple Pay and payments.

Staying on Apple, it is unclear to me as to what is really going on in payments. I hear a lot of buzz around the superior experience of Stripe, Square has IPO’d and I’m not clear what Apple is doing with Apple Pay.

Apple’s lack of commitment to Apple Pay has been disappointing. As an occasional user myself, it is clearly a product with a superior user experience (I’m referring to user experience a lot – more to follow shortly). However, post its launch, Apple has largely been silent on Apple Pay and doesn’t seem to have done much Pay (Ben Thompson has written about merchants complaints on the lack of clarity on Apple pay). And, numerous others like Samsung and Chase have stepped into market with their own versions. The challenge with payments is scale. As you only get a small cut off a payment, you need billions of transactions to make money. This is what ensures PayPal’s profitability – it is a place where network effects are strong. So, to disrupt payments, you need to offer a superior user experience (some would argue that would be easy if it the benchmark is PayPal) and also have the clout to have both merchants AND customers care enough to switch. Apple clearly has the clout. But, a lot more needs to be done.

Back to Apple as a whole.

Another great year for the iPhone, another year when analysts wondered if the iPhone will have a good next year, another year when the Mac did fantastic, and another year when the iPad’s growth was questioned. My prediction is that this will continue next year because none of this is surprising. The iPhone benefits from being the “sun.” We care about our phones, will pay a good amount for it and will upgrade every 2 years. We don’t care as much about the iPad and will probably upgrade every 4-5 years. Not surprising.

Google.

Apple and Google are locked in a war of philosophies. Google is betting on a world where your information on the cloud is indispensable (smart cloud, dumb devices) while Apple is working on the opposite. This war of philosophies was at the heart of the platform wars and will be at the heart of how the internet of things plays out in my opinion. Google’s focus on a smart cloud makes complete sense because it has always been a machine learning company that takes huge amounts of data and spits out a smart recommendation. (Incidentally, Apple’s approach is completely aligned to its traditional industrial design strengths. I sometimes think of this as illustration of the power of influential people in organizations. You could equate these “organization” strengths to those of the Larry & Sergey and Steve Jobs.)

The challenge for Google has been that, despite Android’s domination, engaged, higher value users are on iOS. And, the trend seems to be to switch to iOS as soon as you can afford it. So, despite Google’s market share domination, I would still say Apple has come out the relative winner of the platform wars. Android made complete sense for Google, however. Give the iOS for free and have users on the Google ecosystem who, in turn, feed their massive data engine. However, mobile is less conducive to Google’s search ads based revenue model – the ads are too small on a mobile screen and don’t work as well as on a PC. Additionally, Google faces the same horizontal vs. vertical conflict – does it release a new app for its highly engaged users on iOS? Or does it release on Android first? As I mentioned, this is exactly the sort of issue Amazon faced with the Fire phone. Making the Amazon experience on the Fire phone better goes against the customer centricity that defines Amazon. Horizontal models can’t be made vertical all of a sudden.

To its credit, Google foresaw the change of guard from the web era (where it dominated) to the mobile era. However, things haven’t gone as well as Facebook has cracked brand advertising and social – both of these present problems. First, brand advertising is much more valuable that intent based advertising. And, second, the smartphone is an inherently social device – every app has access to your contacts, can easily share pictures, etc. Facebook nails social in a way Google never has been. So, where next?

The way forward seems to be aggressive investment in whatever could be the next wave. Google’s strengths make it perfectly positioned for the internet-of-things battle with Apple. But, this could just as easily be about cars.

III. User experience matters more than ever.

Old fashioned B2B is declining. I think of this era as the B2C2B era. Great B2B businesses have been built by differentiating on user experience. The adoption of the iPhone in corporates is an example of this trend. The CIO is no longer the sole decision maker on what every person uses. In fact, with “Bring-your-own-devices” becoming the norm, the CIO’s control is trending down (except in highly regulated industries like financial services). As a result, B2B companies that are winning are doing so by winning over customers. A great example of that is…

…LinkedIn. LinkedIn is one of the most prominent (and largest?) B2C2B company in the world. While the revenue streams are B2B, its customer base, at any given time, can only be as large as users who find it useful. A recruiter who isn’t on LinkedIn isn’t going to pay for LinkedIn. So, LinkedIn’s strength is directly proportional to the strength of its users love for it. (Disclosure: I am a “soon-to-be” employee at LinkedIn – so, I’m clearly biased. It is also why I’ll keep my LinkedIn commentary in this post to the minimum.)

User experience in websites was heavily discussed this year.

Users protested loudly about webpages that were being weighed down by heavy advertising. The reason quality content can be made available for free on the internet is because we have advertisers who pay the bills. As you can see from the same chart by Mary Meeker in 2009 vs. 2014, ad spend on the internet has gone up by $50B since 2009.

This rise has been due to the rise of ad networks and programmatic advertising. So, instead of Walmart buying ads on The New York Times, they buy ads on an ad network that has advertising space on multiple websites. So, when you click on a URL to, say, E-Online, the interested publisher checks if it can serve up an ad. The publisher sends this data to a variety of demand-side platforms which weigh up the information (user info, relevance, etc.) and decides how much they would pay for the ad. The ad network then compares the prices and picks the highest price for the publisher. This is simplifying, of course. But, the fact remains that everything you do leaves a trace online and this information is what ad networks use to show relevant ads. All these ads, however, lead to heavier load times and slower webpages.

Buzzfeed is an important exception to this rule. Instead of making money through traditional display ads (which assumes page views matter), Buzzfeed focuses on creating content users want to share and charges brands to sponsor posts or content.

2 initiatives that were created to solve this were Facebook’s “Instant Articles” and Apple’s “News.” They are identical in concept – they offer users a superior user experience by providing news content within their apps/websites, centralize all ad display and share 70% of the revenue with the publisher (in Facebook’s case). This is scary for the publisher because a user now doesn’t need to visit The New York Times website to access it and can spend more time on Facebook, further increasing Facebook’s power. But, it is that or upset users who don’t want to deal with slow load times and will find ways to disable the Javascript code that makes all these ads and tracking possible. Additionally, Facebook’s strength in ads comes from the fact that they target users, not devices (cookie based). With this information, they can serve up better ads. They’re also offering their publishers customization on appearance (so an article from The New York Times will look different from others), 100% of revenue from ads if they choose not to use Facebook’s targeting features, and so on.

Even if the publishers didn’t like the deal, Facebook’s power here cannot be ignored. Very few publishers have the sort of clout that The New York Times and The Wall Street Journal possess. And, even these sites find it hard to generate sufficient revenue from ads. So, if you can’t generate sufficient revenue, your only option is to have more ads. This makes it a big loser in the user experience game and the problem only gets worse on mobile. Facebook, on the other hand, with its excellent targeting capability can actually show fewer, higher value ads (the native ad on Facebook takes up the whole screen.. and, yet, Facebook continues to be as addictive as ever)

The Publishing challenge.

Given zero distribution costs on the internet, publishers can go 2 ways – either build a niche business by maximizing revenue per user or a scale business by making money on maximizing the number of users they reach.

Naturally, these models lend themselves to different business models as well. Niche publications are well suited for either a freemium subscription model with or without really targeted ads while broad publications are more for general advertising. Buzzfeed nails the latter. And, The Economist, in my opinion, is a company that nails the former.

The challenge for most publishing companies is that their business models and incentives don’t align. The fact remains that mobile is very hard to monetize without high quality content. And, very few publishers have the content required to support it. In the face of this, Facebook could be a way out of extinction.. for the time being.

Twitter Moments.

While traditional newspapers struggle, Twitter released Twitter Moments – its first real foray into becoming a modern newspaper. Twitter has been the place where most news breaks out over the past few years. With Moments, Twitter made it official. It even categorized its Moments similar to sections of a newspaper. The content is clearly not a problem – all journalists and newspapers are present on Twitter. Instead, Twitter’s biggest challenge remains new user onboarding and re-activating a whole host of users it has lost due to poor onboarding and limited product evolution over the years.

Moments could be very powerful to the company as it would be able to provide advertisers with very rich data based on user interests. Most sources, e.g. Facebook, assume interest in cars based on a couple of liked pages or posts about cars. If you, however, subscribe to the automobile section of Twitter’s newspaper, it is clear you are a fan.

And, the beauty about the Twitter product is that a product such as Moments, which greatly enhances revenue potential, also improves the user experience. The two rarely go together.

Facebook.

Is there a company whose dominance looms larger over the coming decade? Facebook has many many things going for it – but, top of the list, is the fact that it owns user attention. If man is a social animal, as Ben T says, Facebook seems to be the preferred habitat. Facebook registered 1 Billion daily users this year – that is crazy impressive. Average time spent on Facebook is definitely going up, it has nailed mobile and, unsurprisingly, after cracking the native ad, Facebook is making more money than ever.

The other big factor that will continue to drive Facebook’s growth is that, while Google focuses on direct intent-based advertising (~15% of the total advertising pie), Facebook focuses on brand advertising. The key in the world of brand advertising is user attention. You want your ads to be seen by users. And, it is clear Facebook, and its properties like Instagram, dominate attention and will continue to be “the” place for brands to advertise.

A quick diversion to discuss Snapchat – this brand advertising dynamic is what makes Snapchat powerful too. Rumored to have >200 million monthly actives, Snapchat is a natural place for advertisers to be. The beauty about brand advertising on mediums like Facebook and Snapchat over TV (the traditional brand advertising medium) is that all campaigns come with detailed tracking data. As long as Snapchat and Facebook can hold their user’s attention, their chunk of this pie will only get bigger.

Excellent execution aside, Facebook has also followed Google’s acquisition strategy – strengthen the core and augment by acquisition. Instagram and Whatsapp were fantastic purchases. Both continue to grow and, together, help Facebook dominate the 2 killer mobile apps in mobile – photos and messaging. If this wasn’t impressive enough, Facebook’s own messenger has also had a big year. And, after hiring former PayPal CEO David Marcus to run Messenger, Facebook announced its first “messenger-as-a-platform” move by allowing users to order Uber rides via Messenger. I am not bullish on this working and call it the “WeChat-ization” of Facebook. It is a worthwhile experiment. And, to understand why, we have to understand WeChat and messaging.

Messaging.

Smart phones are inherently social. We carry them everywhere. There will not be one social network that can capture all our social networking activity. We all have many dimensions of our personality and we naturally like to keep our professional (LinkedIn) and personal (Facebook) identities separate, for example. The reason for all these networks to exist and thrive is our need to connect with people similar to us. And, while all these networks enable us to connect with our networks asynchronously (1 to many), we thrive on 1:1 relationships. And, this is where messaging comes into place.

Mobile has made messaging extremely convenient and we, as a result, spend a lot of time on messaging apps. This is because messaging, like email, are social networks in the purest sense. Our email chains and messaging groups contain our most intimate social connections and conversations – and it is with these groups that we do the bulk of our sharing and communication. In short, we move relationships from the social networks like Facebook (which are focused on breadth) to messaging platforms (where we are focused on depth). And, as we have learnt, opportunity knocks in places where we spend our attention.

WeChat.

WeChat is a messaging app with ~600M monthly active users in China that is also a platform. On WeChat, you can do most things you’d want to do “on the go” – order a cab, book tickets at a movie, order a meal, etc. The beauty of WeChat is that it overcomes the app installation resistance – all these services are embedded within WeChat. So, WeChat is not just a messaging app but a “mobile lifestyle.”

These lightweight apps are called official accounts and can be added like adding a friend. For lightweight apps that don’t want to engage with you every day, it makes more sense to launch on WeChat versus develop a separate mobile app. All of this results in monetization through payments. This is the reason WeChat is so interesting – its ARPU or average revenue per user is $7 versus Whatsapp, for example, at $1. The challenge with payments, as I mentioned, is scale – so it is amazing that WeChat monetizes so well. Aside from various promotions and campaigns that got WeChat this scale, it helped that TenCent (WeChat’s parent company) owned many of WeChat’s earliest partners through its seed stage investment engine. And, yes, that’s likely why the ex-Head of PayPal runs Messenger at Facebook.

Using a smartphone in so many ways to do so many things on 1 app has some powerful data implications – if WeChat were Google, it would mean having all your mobile usage information in one place. Imagine what Google could do with that?

Asia’s mobile first dynamics make WeChat a very interesting proposition. Baidu maps is another example of aggregation that has worked in China. In case of Baidu maps, it aggregates location based services that you might want to access once you look at a map – taxis, restaurants, etc. It is hard to predict if this will be the future as it has only succeeded in China – in the absence of vertical giants like Google, Facebook and Amazon. But, it might well be.

Slack.

This special position that messaging holds in the mobile world is what makes Slack and competitors like Hipchat particularly valuable. Slack has been a beneficiary of a couple of shifts.

First, Technology applications generally see a period of bundling followed by unbundling and then back to bundling. After the 1990s where most enterprise applications were bundled by Microsoft, there’s been a lot of unbundling. And, most enterprises use many many niche applications to solve specific problems. Slack is, in effect, is bundling the conversations that involve all these applications in one place. It aims to be the only messaging board you need internally.

Second, Slack’s value proposition is that information is easily searchable and available everywhere. This is critical in a mobile first world. If you’re using 30 enterprise applications, it is nice to know that all information around them are available to you wherever you go. It helps that every enterprise app uses URLs and, these URLs, in turn, make it easy to centralize communications.

(Despite its ease of use on mobile, it is interesting that Slack’s co-founder insists that it is not a tool for mobile-only team. It requires some proportion of usage on a PC.)

Finally, in an age where transparency and open communication is a prized value, Slack makes it easy for employees to easily understand what is going on as history is easily accessible. This isn’t a tool that would have worked in the command-and-control era.

Slack will not replace email but I it will greatly reduce internal email traffic. If Slack continues to win customers with a better user experience, it could be in a great position to be an enterprise platform in the coming decade.

Microsoft.

It is impossible to talk about enterprise tools without bringing it back to Microsoft. It is an interesting time at Microsoft – Windows and Office are, more or less, sources of investments for their cloud experiments. Azure has been growing very quickly and is a credible competitor to Amazon web services. With all its existing enterprise relationships, it isn’t hard to imagine Microsoft playing a big role in the future of infrastructure services.

However, what about productivity tools? Here, it is less clear. It is less clear because a lot of the working world’s work flows are based on tools built for PC’s. And, it’ll be a while before the dust settles and before we see mobile friendly workflows. Slack may be an example of the tool around which the mobile first workplace revolves. However, it isn’t quite certain yet. And, there aren’t credible replacements to Excel and PowerPoint as yet.

TV.

I don’t understand TV as well. So, my notes on TV are relatively short.

TV is definitely a content game. In the past, TV networks have been built around channels like ESPN that have subsidized other less popular ones. Unbundling is where the action will probably lie. iTunes, for example, made it possible for TV show lovers to watch Game of Thrones and The Wire on their laptops (albeit with an annoying delay in case of Game of Thrones). As is a theme with digital, there is very little place for average content. Great differentiated content, on the other hand, continues to thrive.

Over time, it is highly probably that ESPN will break off, à la HBO, and create its own subscription. Digital platforms suit the ESPNs of the world as they commoditize time and enable users to access a wide variety of interesting content (instead of just having 1 game available during prime time, users can now choose between a menu of games on the internet since distribution costs are zero). At the end of the day, content creators own customer experience. Hence, Amazon and Netflix’s foray into content. So, in some ways, the trend in TV is to unbundle the most successful channels and then bundle all good content into them – e.g. get ESPN out and then bundle all good sports content onto ESPN.

Privacy.

Privacy doesn’t really exist simply because everything you do online leaves a digital trace. But, leaving a digital trace is not the same as saying companies like Google and Facebook sell your data (as Tim Cook suggested earlier this year). In fact, the more important advertisements is to a company’s business model, the more protective they are of your data since it forms their competitive advantage. Apple has doubled down on the idea of more privacy and it makes sense. Their strength has always been delivering on the idea of smart devices and a dumb cloud.

Google, on the other hand, has focused on dumb devices but a very smart and responsive cloud. And, for the cloud to be smart and responsive, it needs to have data. While Apple’s approach has worked well so far on account of their superior industrial engineering ability, my prediction is that Apple will need to beef up on its cloud offerings over the next few years if it hopes to be in a good place to win on wearables and internet-of-things. Apple’s approach to privacy hasn’t hindered their ability to build great products as yet – keywords being “as yet.”

How disruption is taking place.

I am going to skate over the ongoing debate led by Clay Christensen (who is awesome!) about how we ought to define disruption. Clay’s thesis is that disruption only occurs bottom up. However, I think Ben Thompson makes a valid point about new age disruption being top – down as adding new customers can be done for a zero marginal cost. However, building a new service still requires a heavy upfront investment. So, companies work on servicing the top end with a great product (e.g. Uber) and then extend the product downward, and then leverage economies of scale to make it more profitable.

Again, all these top end companies win on superior user experience.

Commoditization of trust.

I love Ben Thompson’s insight on the commoditization of trust. Hotels built their brands on the promise of trust. However, the presence of user reviews on all AirBnB property has made this trust redundant. AirBnB has converted every house into a potential hotel and Uber has made every car into potential transport. You could argue that reviews have done the same for online retailing and marketplaces like eBay.

In reality, however, I suspect the sharing economy is built less on people renting beds in homes and more on people who’ve become full time AirBnB renters/Uber drivers. I suspect this will continue to be the case as AirBnB and Uber win more customers on account of their superior user experience.

Aggregating different parts of the value chain.

Ben goes on to provide his take on the nature of disruption today. The change in technology allows us to commoditize different parts of the value chain and integrate others.

For example, Uber broke down the incumbents control of cars and dispatch and, instead, combined dispatch and hailing and payment. Other examples are Netflix which integrated production and distribution and modularized content, and AirBnB which modularized property by integrating trust and reservations.

The key insight, for me, comes from answering the question – who owns customer attention?

While it was okay for hotels to allow travel agents to own the customer relationship, in today’s age, this customer relationship is more valuable than ever before. Again, the differentiation is based on superior user experience.

So, why does user experience matter so much again? In the old world where costs of distribution were massive, manufacturers cared most about distribution relationships and pushed the customer to an after-thought. After all, the distributors owned access. Some examples –

- Game publishing companies like EA controlled access to customers – The app store removed these barriers.

- Publishers used to control aggregation of content into publications. Google made all content modular by providing individual access to web pages

- Book publishers won in the old world because of an oligopoly over distribution. Amazon changed that by allowing customers access to the long tail of products

In each of these cases, the incumbent giants lost because their old edge (distribution) just didn’t matter anymore. Aggregator gate keepers were disrupted because companies like Google broke down what they aggregated. Digitization, as a result, has enabled companies to reach customers directly and has greatly reduced the power of the middle men. New game developers, for example, could now reach customers via Apple’s app store (which owns the relationship and, is thus, most valuable) and capture 70% of their profits. Same with authors via Amazon at the expense of book publishers, companies via Google and Facebook at the expense of ad agencies.

A nice observation from Ben has been that aggregation seems to occur in two stages. In the first stage, you have a pure aggregator that takes all service providers offerings and puts them in one place (Google did that for newspapers, Expedia did that for hotels). But, then, a second aggregator comes that commoditizes all the brands and just focuses on delivering the modular content to the consumer (Facebook did that with news articles, AirBnB did that with hotel rooms). The 2nd aggregators win the market as they are much closer to the customer and much more differentiated.

It is important to note that the effect of this has is felt most by mediocre service providers. Travel agents were expected to be extinct. They aren’t and never will be. This is because awesome travel agents own the customer relationship by providing a superior (human) user experience. Similarly, other great middle-men (e.g. top ad buying agencies) will continue to exist. They will just exist on a much smaller scale and will ONLY be profitable as long as they differentiate by delighting the customer. A great illustration of this “mediocrity-suffers” idea is Adele and Taylor Swift’s refusal to stream their albums on Spotify. Spotify is an aggregator that makes music a commodity. But, when you are as good as Adele or Taylor Swift, you can resist it and, on the balance, do much better for yourself.

This idea is, by no means, a new one. Marketing theory, since Phil Kotler’s time, has emphasized the importance of differentiation. The best way to differentiate is to provide users with great product/service experiences. In that sense, we’ve only gone back to the basics.

A quick detour – first, infinite potential and unicorns.

Compared to the old world, however, the one vital difference is that there are virtually no barriers for a company to own every customer on the planet. There is not much stopping Uber from completely taking over every taxi transaction on the planet. The more users it has, the better service it can provide by having more drivers on the road, better investments in technology, etc. This is why the valuation of network driven companies is massive and is also the reason why we have venture capital firms betting on multiple such companies, making them all “unicorns.” It is, of course, certain that many of these will die. But, investing isn’t a game where you need every investment to be a hit. A few big hits more than make up for the rest of the losses. And, with companies such as Uber, the potential to hit big (regulatory issues notwithstanding) are high.

So, is there a bubble?

Every time this is brought up, we see the usual comparison with valuations in 1999. I think this sort of journalism is lazy. Yes, valuations are high. But, they also reflect the 3 billion additional users who’ve come online since then. As Ben Evans points out, every sensor added on a technology device around us (and, especially, on the ones we carry around nearly everywhere) is a new business. The opportunity is massive.

I think there is no doubt that there is froth in the market. There is also no doubt that many of the unicorns will go bust. But, I expect this to be part of normal course of business and I also expect to see a significant downward adjustment in valuations as interest rates rise. I’m just skeptical of the bubble talk and am struggling to see the basis for it – beyond sensationalist journalism, that is.

2016 and beyond – what we might see.

As the late quote (and baseball?) legend Yogi Berra said – “It is hard to make predictions.. Especially about the future.” Nevertheless, I’ll try.

I’ll start with topics I know little about but that are still important enough to be mentioned and progress to ones where I have more a point of view.

Virtual reality.

Fred Wilson predicts VR’s early launches will disappoint. I can see why he thinks that. VR adoption will take time, for sure. I’m still waiting for my first Oculus experience. Nothing more to say, for now.

Security.

We’ve had lots of conversations about security. It will continue to be a hot topic and a big investment area.

Bitcoin and the blockchain.

There is talk about the blockchain being used more in financial services. I’m not exactly sure how. Bitcoin is definitely being used more than it was before. But, will it ever be a currency to be reckoned with? Also unclear. My immediate reaction to Argentina’s new Financial Minister’s current efforts to fix the Argentine currency is that that might have been a ripe market for Bitcoin to demonstrate its worth. Broken and, yet, visible enough to really spark a discussion. That ship seems to have sailed. Interesting year ahead for Bitcoin investors.

Cars.

There are lots of interesting questions to be asked and answered here. A few things seem certain – at the end of the decade, very few will own cars. Instead, there will be autonomous cars on the road, likely less accidents and a near complete shift to on-demand use. It will be more efficient and better for the environment. How we get there is unanswered. But, the journey (no pun intended) will be interesting.

Internet of things.

My prediction for the internet of things is that it will underwhelm for a few years. While the potential is undoubtedly massive (every sensor creates a new business), it’ll be years before we get this all to work. Creating standards that work across different kinds of devices is a pain. And, in our rush to connect everything to the internet, it is worth asking why as well – why, exactly, should the toaster be connected to the internet? And, is it worth connecting it if the trade-off is to worry about the security patch on the device. More entry points = more security issues => need for better standards which, in turn, is very hard. Besides, this doesn’t even get to user experience – I suspect there are very few people who would be prepared to experiment with a more complicated toaster for kicks sake.

Search and discovery.

Ben Evans asked a great question – what is going to be next for search and discovery on our smartphones? The search and discovery on our app stores is clearly broken. It is hard find new stuff. Instead of seeing one solution/run-time that works for all, Fred Wilson predicts that we will see “contextual runtimes” or multiple runtimes depending on the context. This means that the next lunch delivery app targeted to enterprises will be built using Slack’s API, future ridesharing services will just be built on Google Maps, etc.

This is a fascinating thought – and is one that could just point to the WeChat-ization of the various app constellations we see right now. It could further underline the idea that China’s mobile first behavior was the future all along. App constellations were simply a diversion.

But, why does this matter? This matters because we have way too many apps now for app store lists to work. Curated lists never run out of fashion because there are enough “satisficers” out there who will happily rely on someone’s recommendation and not go through option paralysis. With the internet, there are more options than we know what to do with. And, search relies on us knowing what we want. But, how can we know what we might want? This is the future Amazon and Google aspire to. Big data’s promised future is that we will move from analytics that is predictive to analytics that is prescriptive.

For now, Apple and Google are going at it by curation – think Google Now, Apple Music. So, it is far from figured out and we’re going to try to find other machine learning driven models to make discovery easier. And, until that gets figured out, the main differentiator between services that manage to get adoption and services that don’t is marketing. The infinite range of possibilities has made marketing more important than ever.

(Funnily enough, this is exactly why 99% of folks who start blogs as a side project quit in 6 months. It all looks rosy when you start but it is really hard to build a real following. The only way to do this is to invest in generating high quality content AND spend a lot of time marketing it. And, of course, if you have real work to do in a day, that’s not practical. So, it gets de-motivating really quickly. The only way to get past this is to write for yourself and forget about the audience.)

But, marketing aside, the other way to create an app that has a high chance of usage is to be one created by Apple or Google. Unlike the neutral browser, mobile isn’t a neutral platform. And, that’s obviously worrying if you rely on mobile for your revenues – Facebook is the obvious example. Facebook’s solution has been to acquire services that dominate your attention regardless of your platform (Instagram and Whatsapp). This problem, however, may be exactly why the WeChatized Messenger matters so much to Facebook as both an experiment and a hedge. If Facebook can pull it off, Facebook messenger could become your portal to the world of mobile apps. And, if that doesn’t pan out as planned and if messaging continues to be messaging, well, there’s always Whatsapp.

More mobile and wearable specific use cases.

The challenge with any new technology is that it isn’t always obvious what to do with it. So, the first step is to design by analogy. The first apps on mobile were PC apps for a smaller screen. It wasn’t obvious then that you could build Uber. We are 9 years into the mobile revolution and, many of the mobile relevant use cases, are more obvious now. Still, as this post illustrates, there is a lot that is unclear. It is unclear if we’ll bundle apps into a platform or unbundle them into a constellation, for example. So, more use cases will be tested and more will become “obvious.” However, and this is the interesting part, these will not be about solving technology problems but about solving psychology and human behavior problems. We will move to more convenient and more intuitive.

While this will happen in mobile, I expect this to happen on things like watches as well. At this stage, watch apps do what mobile apps do in a smaller screen. This will change. And, once again, it’ll come down to our ability to understand and tap into human behavior and human needs. This is because technology, at the end of the day, exists to make our lives easier. And, in that sense, the fundamentals haven’t really changed ever since we created the hammer to make our lives better 2000+ years ago.

That’s why – as many things change, a lot of it stays the same.

I guess that’s what makes technology so fascinating.