Every time I read Benedict Evan’s excellent blog, I always tell myself that I’ll come back and read it in greater depth. I finally got around to doing it and went through 2014 from Ben’s eyes and those of a few others. And, I thought I’d share what I’ve learnt. This will be long.

A few notes before we get started.

– First, I’d like to thank our sponsors. The primary sources of this post are Ben Evans and Ben Thompson. Do check out their excellent blogs – 80% of the content of this post is from them. Regular readers of their blogs will recognize a lot of their material and thinking. I am grateful for them for all they do. A big thank you to Fred Wilson and Albert Wenger whose thinking I’ve borrowed heavily on topics such as Bitcoin. Also, thanks to a16z‘s excellent podcasts (which are also on Ben Evans’ blog)

– The next set of sources I’d like to thank are Brad Feld, Mark Suster, Venture Beat, Tom Tunguz, Seth Godin and Vivek Wadhwa.

– I’d also like to apologize for a lack of linking in this post and a lack of images. Given the amount of data in this post, linking or adding images would have driven me crazy. Sorry about that.

– Finally, I’d also like you to note that I’ve done my best to aggregate their thought and infuse a few of my own. The flow is just what felt right as I put these together. I’m sure there are a few mistakes and typos along the way – not just in the data but in the many assumptions that are inadvertently made through the post. Please let me know when you spot them.

2014 – the year tech outgrew the tech industry. One of the ideas Daniel Ha, CEO of Disqus, shared in a RealLeaders.tv interview that there will come a time when technology is taken for granted just like electricity is. We don’t call companies electrical companies as we did 100 years ago. This was the year we saw companies like Buzzfeed (media), Tesla (cars) expand the boundaries of technology. Technology will soon be central to what we do.

We’ll start at data from Christmas 2014 shopping in the US

– 8.3% increase in e-commerce over last year

– Mobile made up for 50% of online shopping browsing, 34.8% of online sales

– iOS users spent $97.28 per order while Android users spent $67.4

– iOS drove 39% of total online traffic with 27% of online sales while Android only drove 17% and 7% of online sales

– Facebook referrals drove an average of $90 per order while Pinterest referrals averaged $100 per order

As you can see, there’s a clear difference in the shopping behavior of the average iOS user vs. the average Android user – even in the US.

Let’s dig deeper into the iOS vs. Android difference

The split between Android and iOS is as follows

– Phones -> 82% Android, 14% iPhones

– Tablets -> 68% Android, 28% iPads

There is clearly higher wealth on the iPhone

– Black Friday 2014 – iOS had 78% of sales while Android had 22% of sales

– Christmas 2014 – iOS drove 27% of online sales (as per data above)

In terms of devices, iOS has 650M devices, 1.3B Google devices (please note that numbers around these are always approximate)

– However, Apple paid out $10B to developers while Google paid out $5B

– Clearly, developer revenue is pretty concentrated on iOS

– Even though Android – primarily Samsung – has a share of the premium Android market, it seems Apple is generating more money per user

– The rough split of mobile devices overall – 10% high end iOS, 10% high end Android, 40% iOS

The iPhone 6 was a move against premium Android (half of premium market) while the 6+ was against phablets.

– Hence, iPhone 6 pretty much spells the death of Samsung, who were already being squeezed by other Android OEMs from the middle

– Samsung not helped by significant lessening differentiation between iOS and Android. Additionally, OEMs like Xiaomi are definitely taking away share.

Difference between iOS and Android is in the overall strategy and that has a lot to do with the identity of the 2 companies –

– Apple has its focus on dumb cloud and smart devices while Google is all about the smart cloud

– Apple can focus intensely on the devices because they control the whole stack

– Google, however, doesn’t, and it needs to innovate in the cloud

– Both of these suit their identity as companies – Google is a machine learning company which has built a smart learning machine (the cloud) while Apple has created devices that delight customers

Both Apple and Google have won the platform wars..

– Even if Android has 1.3B devices, Apple is far from the loser. 650M devices is no mean feat and they make most of the money

– However, with both Google and Apple winning, the duopoly is potentially stifling innovation. For example, developer incentives are all over the place. Apple doesn’t allow built-in upgrades => developers are discouraged from creating complex apps that may unlock the true potential of an app – hard to create real value add when everything sells for 0.99.

– Also, discovery is very hard. The web was neutral and Google introduced pagerank to help us search it. But, there is no pagerank equivalent

– Apple & Google have tremendous power as platform owners in figuring out this next step.

– And, while we have a lot of reasons to criticize Apple and Google’s moves in controlling their platforms, it has got to be said that the app stores have gone a LONG way in democratizing innovation. As a dear friend who has runs his own game development startup points out – they get to keep 70% of the revenue from their game. This was not possible before..

Now, how about some more on mobile

– For the first time ever, a piece of technology is now sold to nearly every adult on earth. This is unlike the previous eras of Microsoft, Netscape, and Google

– Approximate numbers – 2B phones sold per year. 10% – Apple, 50% Android split between 33% Google Android, 17% Non-google Android

– There are only 1.5 Billion PCs in total – Microsoft’s share of total personal computing devices has fallen swiftly from ~100% to around 30%

– 200M smartphones in the US, 700M in China

– We are heading to a world with 4B smartphones on earth

– Also, an iPhone has 600x more computing power than a 1995 Centium. That’s significant.

We’re still really figuring out the mobile opportunity

– The more sensors there are, the more the phones know about us => the more the opportunity

– The biggest difference in web vs. mobile – in the web, you could link to anything and you could get it without downloading it. Mobile is different.

– As a result, mobile innovation has proceeded in different ways. In most countries, large tech companies have focused on unbundling their web versions and providing app “constellations,” e.g., Facebook has many Facebook apps that do what its web version does

– In China, however, Baidu and Wechat offer bundled experiences. Baidu has many booking services along with its map services – it seems them all as related to location

– A sense of scale – Whatsapp does 7 Trillion messages a year – similar to global texting volume. And it did it with 30 odd engineers.

– Also, there were 800 Billion photos shared this year (=> more were created). 80 Billion photos was the peak for film in 1999

– Facebook generated $3B in mobile ads after about a year of experimentation in mobile ads. The potential is HUGE.

– Facebook wants a meta OS that connects its constellation (so it doesn’t depend as heavily on Google and Yahoo.) But, there’s all sorts of problems because the value of iOS and Android lie in their app stores

Amazon Fire phone and the difficulties with Google Forks

– Amazon’s Fire phone was the first serious attempt at a Google Fork, i.e., using Android but attempting to create its own app store

– This is important for companies like Facebook and Amazon – again, the browser was neutral. The app store is not.

– The app store is a great example of strategy that reinforces the platform owners – Apple and Google

– Amazon’s Fire phone hasn’t worked as yet. Was it to appeal to a small bunch of Amazon’s most loyal customers? Was it to test if Amazon has the muscle to create a developer ecosystem.

– It was an important shot – there are arguably just 3 companies (Amazon, Microsoft, Facebook) that can experiment with a move like this and hope developers will follow them.

– It is unclear what the long term play is with this. And, you can bet that Jeff Bezos has a long term vision. Either way, stay tuned for more.

While we’re at it, let’s talk Amazon

– Amazon reports that 10 million members tried Prime this Christmas

– There were 10 million members in March 2013 – could the current number of users be around 40M?

There was a lot of noise made about Amazon’s profits. Let’s first look at some numbers

– e-commerce is roughly 10% of total North American retail

– Yes, Amazon reported $75B in revenues last year, but Amazon is only 1% of North American retail. Why on earth would a CEO who is thinking long term not use its earnings to pursue more of the opportunity? (Additionally, reporting profits => more tax costs)

– The only way you can get a $0 profit every year is if it is intentional. Clearly, there is a finance team tasked with doing this. The remaining money is pumped into growth engines – warehouses, AWS, etc.

– From Jeff Bezos’ point of view, the main utility of the share price is compensation since Amazon compensation is loaded with options. So, as long as he can keep it stable, he can go back to playing the long game and focusing on investors who are in it for the long term..

Some more Amazon numbers

– Physical media like books account for ~25% of their revenue but almost all of their “profits” (rumored)

– The rest are a mix of profitable and unprofitable companies – Amazon truly is a conglomerate, not a retailer

– Operating cash flow margin has stayed at 6-8% of total revenue

– “Other” category or AWS is showing hockey stick growth

3rd party sales at Amazon is about 40% of all units sold and 20% of revenue

○ Note – Amazon revenue ONLY reports the commissions on 3rd party sales – so, $75B is not the full value of goods that pass through Amazon

○ This also means Amazon doesn’t control the price of about 40% of what is sold on Amazon since it is fixed by 3rd party sellers.

It is remarkable how Jeff Bezos has built a company that is so true to its principles. To really understand Amazon, we have to understand the famous Amazon flywheel that Bezos once drew on a napkin

(Note: nowhere does it mention profits :-) Another note – Ben Thompson accused me of being too bullish on Amazon in our email exchange. Guilty as charged. I am definitely biased to Jeff Bezos. :-))

After a brief Amazon detour, let’s go back to mobile Telco’s and messaging

– Telco operators have had a number of existential threats, e.g., Whatsapp beat global SMS and took away a major source of revenue, Skype did so with international calling

– Telco still requires massive investments to secure bandwidth but pricing is still a huge problem. The biggest challenge is to move from old-world pricing to new-world business models

– Interestingly, identity may be the next big challenge. Telco’s still have a stake in your “identity” as the phone number attached to you. That is a part of the “lock in” / differentiation. But, if the phone number no longer serves as identity and you only buy data (or you buy Google Voice), what happens next? The less the differentiation => price wars

As we’re discussing big industries swept by technological change, let’s spend a couple of moments on Music

– Recorded music sales barely makes $17B. As comparison, the iPhone generates $25B in a quarter

– Content is clearly no longer king in music. The hardware is, though. Hence, Apple’s acquisition of Beats at 3B could make sense – it isn’t about the music but the headphones you listen to them in.

A quick note on the Spotify vs. Taylor Swift

– Spotify is indeed hugely beneficial to many many artists – they’ve paid out $2B to artists, after all

– However, Taylor Swift is an artist who has, in strategy terms, large amounts of “added value.” Added value is the value that disappears from the ecosystem when she disappears. More added value => harder to replace => high profits.

– In her case, she was clearly not capturing enough of the profits and her move away from Spotify was perfect for Taylor Swift

– It could, perhaps, be an indicator of what Spotify might be in the future. Perhaps successful artists will “graduate” from Spotify and its real value will be as a discovery engine?

The internet’s middle man problem

– In general, the internet has not been kind to the middle man (just ask travel agencies). Spotify is a different sort of middle man. It is built on the internet and thus adds value (for most artists). (Taylor Swift is exceptional and deserves exceptional treatment)

– But, famous radio personality Ira Glass’ move from the radio to internet further demonstrate the simple idea – the upsides can be huge if you are irreplaceable

– Amazon’s fight with Hachette is an example of just this. The old world publishing model just doesn’t work and books need to get cheaper. Jeff Bezos correctly sees all sorts of media (music, videos, etc.) as competitors to books. Publishers can’t continue to charge so much overhead.

– Given the resources available, writers who have a following will go ahead and self-publish anyway (see Seth Godin’s latest book as an example and his Kickstarter campaign for his previous book)

A quick turn to Communications

– The average US subscriber spends 1250 on all communication. Ofcom has data for many leading countries

– ~80% had a smartphone and laptop in most of these companies

– What was notable was massive spikes in in China for the number of people who’ve made mobile payments – 60% vs. 30% on average in other developed markets

– Internet share of overall advertising spend up between 35-40% this year, growing at 4% per year

– Finally, the average number of hours of TV watched /day is still around 4.5 hours per person (if you find that as shocking as I do, clearly we don’t have as firm a grip on the “normal” person)

Television

– The 4.5 hour per day of attention given to TV still captures the imagination of entrepreneurs all over

– The difficulty though lies in producing content. In TV, the flywheel is Audience -> Revenue -> Content -> Audience.. And content takes huge capital costs

– For example, Netflix is attempting to move from movie screening to live content e.g. House of Cards. But, House of Cards costs $5M or more an episode

– Hence, Disney paid 500M for Maker Studios for good YouTube content

– There are many big questions thought – is TV set for an iTunes like unbundling? What if you break it down to shows – how will it change when you can just choose which shows you want? What happens to the rest?

– Can Apple succeed with Apple TV?

Speaking of Apple – let’s discuss Apple Pay..

– Apple has consistently built products by rolling out features incrementally for other use cases. For example, the fingerprint scanner was released as a way of unlocking the phone. But, it is clearly critical to Apple Pay

– Apple is partnering with banks with Apple Pay – and not competing. This is a FANTASTIC example of strategy – Apple’s partnerships/contract agreements are an example of when not to attempt to “integrate.” While Google attempts to take over the world, Apple sticks to a key tenet of strategy – only acquire a new business when you can do something with the business that the current owner cannot

– Apple has no interest in becoming a bank or credit card. So, it partners with them. But, with a move to payment software, it can still be pretty dangerous for incumbents (just ask the music industries or telcos)

There are many possibilities with Apple Pay

– There are possibilities for within app purchases – if it allows other apps access to one-tap pay => more money in the iOS ecosystem => better developers (we’ve already discussed why this matters – the platform is key)

– In terms of point-of-sale payments, there are 4 players that matter – Apple customers, credit card networks, banks, and merchants. Out of these, Apple has partnered with credit card networks and banks – so, they all love Apple Pay.

– However, merchants don’t see a use case as yet. But, if NFC technology becomes the standard in all terminals, Apple Pay will become an obvious customer need.

– And, given, enormous loyalty from Apple customers, it is likely that merchants will bend..

A quick note on Apple Watch

– Hard to predict the possibilities as with any new technology – could be a luxury play with “delight” at the centre of it?

– The big question probably is – what can developers do better on a watch than a phone? This will drive what it could be. At this point, it could just be a hobbyist accessory. But, it could just also be the future smartphone..

Wearables and wellness

– Wearables are definitely going to be a big part of the future. Since I’m not focusing much on speculation, I won’t say much more except that cracking wellness is going to be a key priority.

– The principle here is that the more sensors we have in convenient places, the more the opportunity to do stuff that matters

– Wellness is an example of that. The more data we have on existing health habits, the more we can focus on preventive care..

– It is all going to come down to data.

Big Data

– We’ve moved through 3 eras in terms of technology – Descriptive era to the current predictive era and all bets are on entering the prescriptive era where technology will use our data to tell us to exercise (for example :-))

– There are 40,000 Exabytes of data expected to be generated in 2020. 1 Exabyte is 1 Billion Gigabytes. More data will be generated in 2020 than probably ever before.

While we’re at big data, let’s look at Google

In case you haven’t noticed, Gmail is being redesigned despite huge outcry within Google

– The reason is that the average Gmail user only receives 5 emails per day – mostly promotions. So, the inbox app is designed for the average user

– The plan for now is to keep Gmail with all its power features but to focus it now on their real ‘normal’ user Only

What is Google up to?

– Google is clearly wondering that itself. News that there were only about 100M Google Map users raised many question about the power of Google services. Are Google services as critical to its strength as we think they are?

– Google’s search is clearly the best. While Bing and others may chip away, Google’s search and search ads business will be the winner. However, the era of the search ad is likely to be eclipsed in the coming years with native personalized ads

– Google doesn’t do as well with native ads that Facebook, Twitter, etc., do great at.

– A quick note on Twitter – there has been a lot of mumbling among investors around Twitter. While I am unclear about the role of their management teams, Twitter still seems to have trouble articulating its value. It works – that much is clear and it’ll continue to work as a secondary social network to Facebook. But, will there be more?

– The big question, then, is if we’ve already seen peak Google? Because, by missing native, Google has probably missed the huge monetization opportunity in mobile (Android is free and its store doesn’t make as much money).

– Will Google just skip the mobile wave and aim to make it to the next wave with their many moon shots, e.g., consumer devices like Nest and self-driving cars?

Cars

– Google apparently is looking for industry partners for self-driving cars. Interesting move given their usual habit to just chip away at a new industry by doing it themselves. This is more of an Apple-esque move (as detailed above).

– This is probably the smart thing to do as the cost of bringing this technology to market can be substantial given regulatory burdens and acquiring new expertise.

– Meanwhile, Elon Musk continues to make waves with Tesla. Tesla’s approach seems to be to focus on hobbyist while working hard in the back end to make sure the technology is cheaper by 2017

Speaking of searching for the next big thing – Facebook bought Whatsapp for 19 Billion

– Zuckerberg’s thinking was simple – 450M people were spending time nearly every day at Whatsapp. And, he felt they should be part of the Facebook conglomerate along with Instagram and other services.

– Whatsapp simply unbundled a part of Facebook (messaging)- Facebook has gone on building its constellation of apps by unbundling itself

– Key question as in any acquisition – can Facebook do more with Whatsapp? Potentially, the answer is yes. First, Facebook can allow Whatsapp to continue down the growth path without worrying about monetization. Second, it also makes more sense to buy a competitor that is hitting it big than trying to build it yourself. Where social is concerned, there’s a huge element of luck involved.

– And, speaking in $, the deal valued the active user at 35, similar to what Google paid for at YouTube. Most of the shock was due to Whatsapp’s small team size. But, we’ll have to get used to that in the age of mobile.

– Whatsapp hasn’t won messaging though. There are numerous regional competitors like WeChat and Line. It is still a dominant global player.

– Facebook has done well in the mobile phase of technology. But, it is unclear what’s next. They’re aggressively trying to find it though with their acquisition of Oculus (virtual reality).

Another area in search of the next big thing is Productivity

– First, productivity is a hugely emotional topic and takes a long while to change

– Excel and PowerPoint likely to remain dominant for a while as work products take a while to change.

– Excel and PowerPoint have had SO many use cases – e.g., Excel was the preferred word processor in Japan because it was super structured while presentations are often done in Word in banking

– There are SO many use cases that we now have apps that handle separate parts – task lists, event organization, etc.

– The way data presentations are done have also changed because data is now up to date and shared online. Now, meetings are around discussions about data..

So, what of Microsoft?

– Helps if you think of 2 Microsofts – the consumer/”device” Microsoft which has devices like Xbox, Surface, etc. and the enterprise/”services” Microsoft that has services like Office, Azure

– Enterprise Microsoft doing exceptionally well – Windows, Office, Exchange have continued to do well. Office 365 and Azure are growing very quickly.

– Windows 8 has largely failed. So, Microsoft is working hard on producing next gen windows which its enterprise customers can get on board with

– But, consumer section struggling with Xbox, Bing, Surface etc.

– Satya’s strategy of “platform and productivity” has clearly changed things though. He seems to be focusing on the enterprise part by moves like offering Office apps for free (partly) now.

– Speaking of platforms, the Minecraft looks really good – a game with a very loyal install base and a true “platform”. And, Microsoft can do a lot more in terms of expanding Minecraft’s reach and influence with its might behind it => good strategy

Box, Dropbox – the storage wars – and perhaps Microsoft?

– As we were discussing Enterprise Microsoft, there have been a few interesting developments here in terms of storage

– Dropbox has firmly moved into the enterprise business with Dropbox for Business. But, it seems to be primarily focused on SMBs. This is, of course, different from where Dropbox’ traditional strengths are (consumers). Microsoft seems to be moving to work with Dropbox in some way (Satya Nadella is really changing things)

– Box.net, on the other hand, has delayed its IPO a couple of times as it seems to be on a drive to fix its costs to acquire users numbers. Latest S-1 filings indicate an impressive turnaround in these stats

– The fact still remains that Box.net has invested heavily in what it considers a “go-big-or-go-home” battle. But, is the battle with Dropbox alone?

– In the long run, storage will get cheaper. But, data is still valuable and it looks like they have their eyes on Microsoft’s enterprise services business. Satya’s move to focus on becoming cross platform must not have been celebrated at Box headquarters.

A more technical look at the back end – Containers

– Containers in technology work with the same concept as shipping container. It doesn’t matter what is inside the container but it should just work on any Linux based service, e.g., AWS, Azure

– Containers work when they are open sourced (the design for the shipping customer is open sourced and enabled all container companies to build according to it and then make it the standard) and Docker was critical in this. They help developers not worry about different frameworks, versions, etc.

– The question now is if Docker can monetize and build a sustainable business

– This has numerous implications for virtualization because containers are more efficient than virtual machines because virtual machines each have their own OS, etc.

– Interestingly, Docker containers in virtual machines can make for an even better solution as, while Docker containers help with highly scalable applications, virtual machines have their own list of merits – security, ecosystem, etc.

– VMware has moved to announce integration of containers into its stack of products. This could just have been a defensive move given many industry observers tout containers to spell the death of virtualization. It is probably not the case..

A few quick notes on a bunch of other topics –

2014 saw increasing policy related battles. As technology continues to disrupt incumbents, we can expect much much more of this. Some areas were

Net Neutrality – where lobbyists from the telecom and cable industries tried to exert control over the internet and what their consumers saw

Immigration in the US – I have too much vested interest here. So, I will pass on this.

Uber and AirBnB vs. policy makers – This is a recurring theme and we should expect to see more

Uber

– Has developed an incredible position to dominate same-day e-commerce and increase driver utilization around the world

– Aggression is required on their part because being the winner takes a big portion of every market. But, it remains to be seen if they will mature into a company that learns to be a good “big dog”

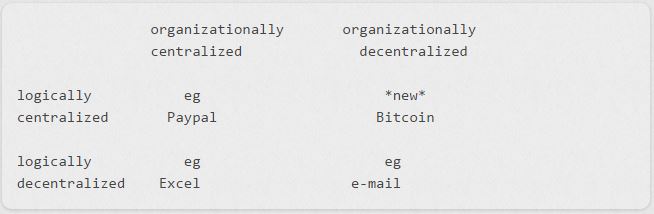

A note on Bitcoin. It is impossible to talk about transformative technologies without touching on Bitcoin. For all those confused about Bitcoin, I thought I’d copy Albert’s fantastic post on the topic

The “organizationally centralized” column on the left contains systems that are controlled by a single organization (EBay and Microsoft in the examples, but this doesn’t need to be a corporation, it could also be a government). Conversely the “organizationally decentralized” column on the right contains systems that are not under the control of any one entity whether for profit or otherwise.

The “logically decentralized” row at the bottom contains systems that have multiple databases and in which participant controls their own database entirely. For instance, when you send me an Excel file and I now work on that on my machine I only make changes to my copy. You and I can work on entirely different Excel files without them ever being connected to each other. Even with email we each control our separate databases. For instance, I can delete a message that you sent me and that doesn’t delete it in your “sent” box.

Conversely the “logically centralized” row on top contains systems that appear as if they have a single global database. I say “appear” because technologically there could be many separate database systems involved. What “logically centralized” means is simply that anyone in the world gets the same answer when querying the system.

The important innovation provided by the blockchain is that it makes the top right quadrant possible. We already had the top left. Paypal for instance maintains a logically centralized database for its payments infrastructure. When I pay someone on Paypal their account is credited and mine is debited. But up until now all such systems had to be controlled by a single organization.

Let me repeat that again for emphasis: before the blockchain’s existence there were *no* systems that were organizationally decentralized, yet logically centralized. This is why Bitcoin is such a foundational technology. When I send Bitcoin to someone then both the debit and the credit are recorded in the blockchain even though that database is not controlled by one organization. As it turns out, this means that many other applications that require a single global database can now be created on top of the Blockchain Application Stack.

(E.g. OneName.io has created a distributed identity – identity not controlled by any one startup but that is built on top of the Bitcoin blockchain.)

What we could be seeing – My view

We’ve seen different eras. Ben Thompson describes this in 3 epochs personal computer -> Internet -> Mobile -> whatever is next. This has resulted in a few interesting trends.

In all content industries, we could be seeing a big concentration in resources at the very top. There is tremendous money in differentiation, perhaps more than ever before. And, then, there’s the other side – you don’t need to be a behemoth to be wildly profitable. You just need to provide top quality services to a collection of “fans.” The internet has enabled you to do that. (See Seth’s blog for more)

If you look at how civilizations have progressed over time, you notice that the center of the world has shifted a lot. It started with the fertile crescent in modern day Iran and has moved westwards to the US. At each turning point, what was a strength in the previous stronghold became a weakness. It is the same with big tech giants. We see each of them struggling with a similar kind of problems. Microsoft’s strength with Windows led it to believe that mobile could just be an extension of Windows. Google and Apple, on the other hand, built it from scratch. Similarly, Google’s domination is search ads meant it wasn’t well positioned for native. Google+ doesn’t work nearly as well as a Facebook that built it from scratch. That is not to say big companies can’t innovate. It is just that it is very hard and against their current incentives.

It is my belief that the age of social media entrepreneurs is nearly done. That means there is a good chance we will see older and more experienced entrepreneurs. Entrepreneurship, as a concept, generally requires domain expertise. Youngsters had tremendous domain expertise in the area of social media and connection. Youngsters are generally in the ‘building connections’ phase of their life while the older groups have set social groups. Twitter, Facebook, etc., were often built by tech-savvy youngsters who craved social connection. The next wave of disruption, in my view, will take either deeper tech chops (by leveraging the blockchain or technologies like it), domain expertise (people who understand what it takes to disrupt industries like energy or healthcare) or a potent combination of both. Intuit, for example, has illustrated this. Despite its size, it has moved nimbly to strengthen its hold on managing personal finance. A focus of that sort can be incredibly powerful. That’s not to say we’ll need less social media or community – community will just be foundational. Intuit’s focus on personal finance doesn’t remove the need for Intuit to focus on community. In fact, building its community of small business owners is among Intuit’s key strategic priorities.

We’ll see more of science and the arts. Apple and Steve Jobs made this analogy popular. But, this has been the case since the early days of technology from when Ada Lovelace first wrote about technology in her writings about her collaborations with Charles Babbage. Here, Adobe, for example, has been chipping away behind the scenes at a potential intersection of providing creative tools to creatives around the world and marketing tools to marketing managers who then decide where the creative work should be displayed.

As I write this, there are thousands of startups working on creative solutions around many of the ideas mentioned in the post as well as many others I haven’t even been able to imagine. That’s what makes the world so exciting.

2015 will be another big year in technology. We’re just getting started…

PS: As I mentioned right up top, this was indeed very long. I hope it was worth it…