I’ve been thinking about the macroeconomic environment in the US of late and shared the update below as part of a weekly update I send at work.

(1) What is happening?

(i) We are in a “bear” market with a >20% hit to equities – with more significant hits in tech stocks – but it is also important to view this market with some perspective

At some point in the past months, you’ve seen a chart that looks something like this.

There is no question that those decreases are significant – a 75% decrease in stock price will require a 400% increase to get back to previous highs. But, instead of us focusing on that, I’d like to show a different view.

Warren Buffett once said that his favorite market valuation indicator is the total value of the U.S. stock market relative to what the U.S. as a country produces, otherwise known as Stock Market Cap to GDP. So let’s take a look at that. This chart tells us something different – on aggregate, we’ve gone from very overvalued to somewhat overvalued. In short, what seems like a totally crazy market movement is just a journey to normalcy.

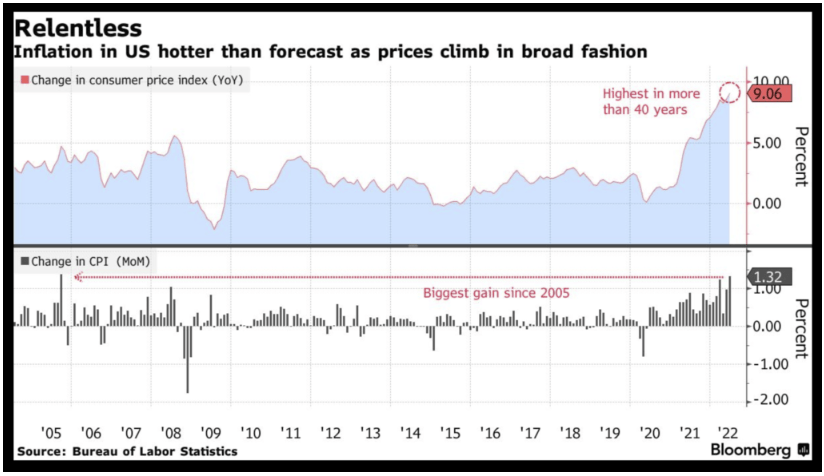

(b) There is also a large increase in inflation and the consumer price index. It is this increase that is the cause of the worry. Inflation is higher than it has been in 40 years.

This increase in prices will have many ripple effects – one with consequences to the labor markets is early retirees from 2021 ad who moved out of the market early deciding to come back to work in 2022.

But the most consequential of these is the Fed’s response by increasing interest rates.

(c) A combination of the decline in stocks, high inflation, and rising interest rates has resulted in two kinds of effects we’re seeing plenty in the news – (a) hiring freezes and (b) impact to private markets

(a) One the one hand, you’ve seen headlines like this signaling hiring freezes

The key takeaway is that every leader is being cautious about their approach going into the next 12 months given the uncertainty in the macro environment.

(b) On the other, we are also seeing significant changes in the private markets (which typically follow public markets with a slight lag)

Here are 3 telling stats (the first 2 are thanks to Pitchbook’s VC report)-

- IPOs cooling down: There were 183 VC backed IPOs in 2021 and 108 in 2020 (with the pandemic related slowdown between Mar-May). There were only 22 in the first half of 2022.

- Lots of M&A: While Mar-Jun 2022 saw the lowest exit value since 2016, exit counts remains high. This means we’re seeing lots of deals <$500M as start-ups run to shelters and acquirers take advantage of bargains

- Significant valuation write-downs: As is expected given the public market takedown, we’re seeing significant write-downs in start-up valuation

(2) Now that we’ve talked a little bit about what is happening, let’s ask why?

Again, let’s cover stocks, inflation, and the impact to hiring/private markets in the same order.

(i) From a historical perspective, stocks and commodities have gone up whenever central banks print money

For a more detailed primer, Ray Dalio’s video on “Principles for dealing with the changing world order” is a great watch.

Overall, when the central bank prints trillions of dollars in response to a crisis, the value of paper money falls and the value of stocks rise.

(ii) Inflation shocks are typically caused by a rise in demand increases and supply costs

We experienced a bit of both in 2020 and 2021. With all the wealth flowing into the economy with stimulus gains, there was more income to buy goods (vs. services which suffered given social distancing mandates). Production had slowed given the pandemic => we experienced a pandemic-driven supply chain crisis.

We’re also seeing more of that in 2022 driven by a new variable -> The Russia-Ukraine war. That’s both because the European Union is very dependent on Russian gas….

…and the world is dependent on both countries for wheat (a staple food) – among other things.

(iii) Given these forces, the caution in the market makes a lot of sense

There are two reasons for this caution:

- When interest rates are low, borrowing is cheap. When borrowing is cheap, the story of the future matters a lot more than the story of now. However, when borrowing becomes expensive, we have to be very discerning about our investments given the opportunity costs. So, it makes sense that everyone is collectively turning the dials toward profitability over growth. This was especially the case in tech – as start-ups and crypto benefited tremendously from huge influxes of cheap capital.

- There’s uncertainty around how the next 12-18 months will pan out. So, if you’re a start-up burning lots of money, survival is first on the agenda.

(3) What comes ahead?

(i) Nobody knows (it’s important to start here)…

Here’s a recent quote that helps explain this best – “I think we now understand better how little we understand about inflation.” | Jerome Powell, Chairman of the US Federal Reserve / probably the most consequential person on the planet with respect to global financial markets.

(ii) There are reasons to believe we’re at the cusp of a possible recession or stagflation where we see stagnant growth and inflation combined.

This is a consequence of the significant increase in interest rates. More interest rates -> more interest costs to pay off. This typically results in a slowdown in growth.

Borrowing creates these cycles – more in Ray Dalio’s excellent video on “How the economic machine works.” His recent LinkedIn article explains why stagflation is the likely result of the Fed’s recent moves.

In his words –

“Central banks should:

- use their powers to drive the markets and economy like a good driver drives a car—with gentle applications of the gas and brakes to produce steadiness rather than by hitting the gas hard and then hitting the brakes hard, leading to lurches forward and backward.

- Keep debt assets and liabilities relatively stable and, most importantly, not allow them to get too large to manage well. To do this they should not allow interest rates and availabilities of money to be either too good or too bad for the debtors or the creditors.

By these measures central banks policies have not been good.”

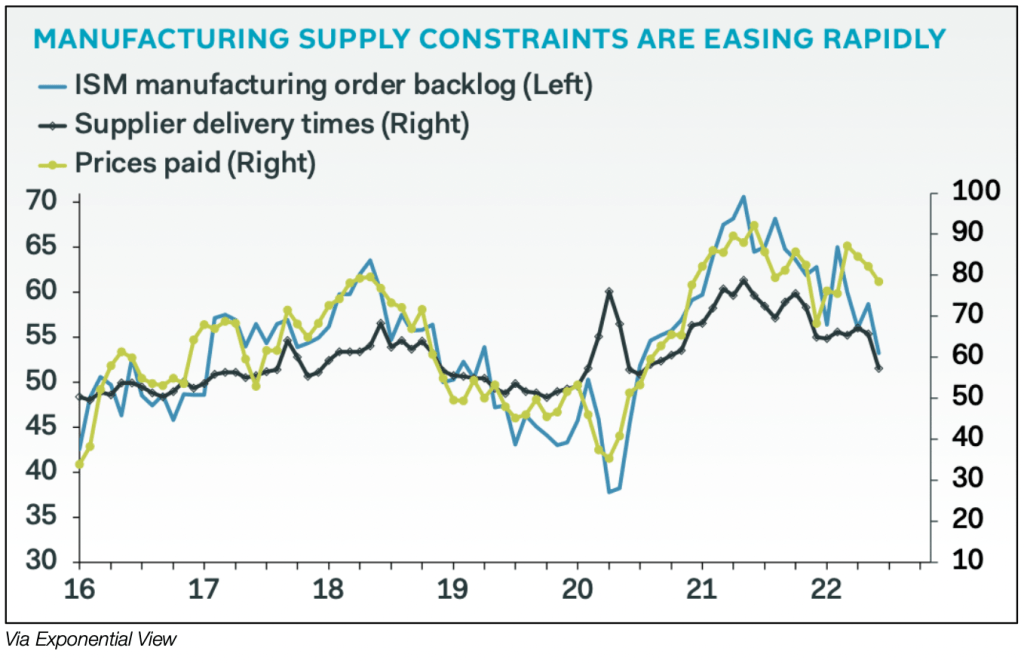

(iii) But, that said, there are reasons to be optimistic thanks to one piece of the puzzle potentially coming back to normal – supply.

As you can see manufacturing order backlog globally is coming down after highs in 2021.

The price of GPUs/specialized chips – as an example of an issue – is getting back to normal

Inventories are growing after a significant dip in 2020 and 2021.

And oil prices – which have been elevated – are on their way down.

The big question then – has inflation peaked at 9.1%? If these indicators hold, there is a chance that will have happened. And that will signal a significantly more optimistic shift in how we think about the situation. We’ll know more next month.

(+1) What does this mean for us?

Switching back to an internal lens, here are the 3 things that come to mind –

(i) It helps to keep perspective

The correction in stocks so far has just taken us back to where we were in late 2020. It’s crazy to think just how much stocks rose in the past 2 years. This correction is long-term healthy.

And it is just a blip on a 30 year horizon – one among a collection of similar dips.

So, keep calm, maintain perspective, and stay diversified and safe out there.