Scott Galloway shared a post last week about a topic I’d been curious about – “Buy Now Pay Later.” It’s been fascinating to see firms like AfterPay featured prominently in checkout flows. I was curious about how these firms are different from a loan or from plain old credit card debt.

Turns out they aren’t. The whole post is worth reading in full. I’ve copied a few excerpts below.

The stale product formerly known as a loan has been rebranded as “Buy Now Pay Later,” or BNPL. The premise is simple: Buy a product for a fraction of its cost at checkout and pay the rest of it off over a few weeks or months. The good news: Debt is not as bad as cancer. Though it can trigger depression and even revolution. But that’s another post.

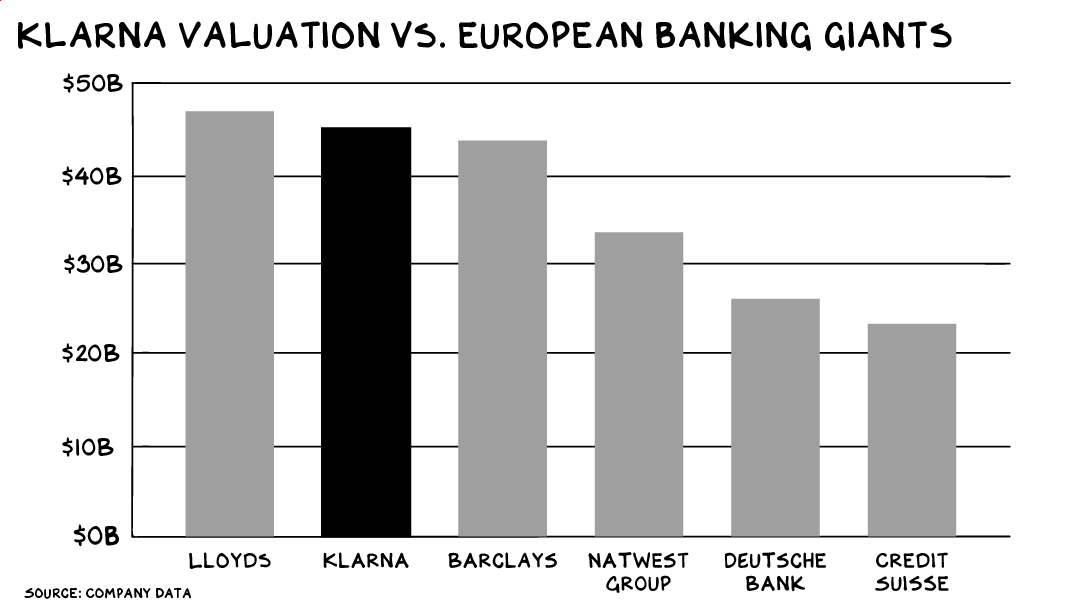

BNPL is one of the hottest trends in finance: 1 in 5 Americans used one of these services in the past year, with U.S. spending on BNPL increasing 230% since 2020. By 2025 global BNPL spending is projected to double to $680 billion. In August, Square acquired BNPL pioneer Afterpay for $29 billion in the largest-ever acquisition of an Australian firm. (We had the Founder/CEO of Afterpay on the Prof G Pod, and he’s an impressive young man.) Swedish BNPL giant Klarna is getting ready for a $50-billion-plus IPO, with a current valuation on par with ING or Lloyds Banking Group.

The target market is young people. Klarna’s frontman is rapper A$AP Rocky (who was paid in equity, not debt) — many BNPL brands rely on social media influencer campaigns. In the U.S., three-quarters of users are Gen Zers or millennials; it’s projected that nearly half of Gen Z will be using BNPL services by 2022. Their attraction to BNPL coincides with an aversion to banks and the credit they offer. This is a generation that came of age just before or in the wake of the Great Recession, a global economic crisis precipitated by … way too much credit. Young people love BNPL because, according to the former director of Afterpay, the vast majority of them “don’t want to be on credit.”

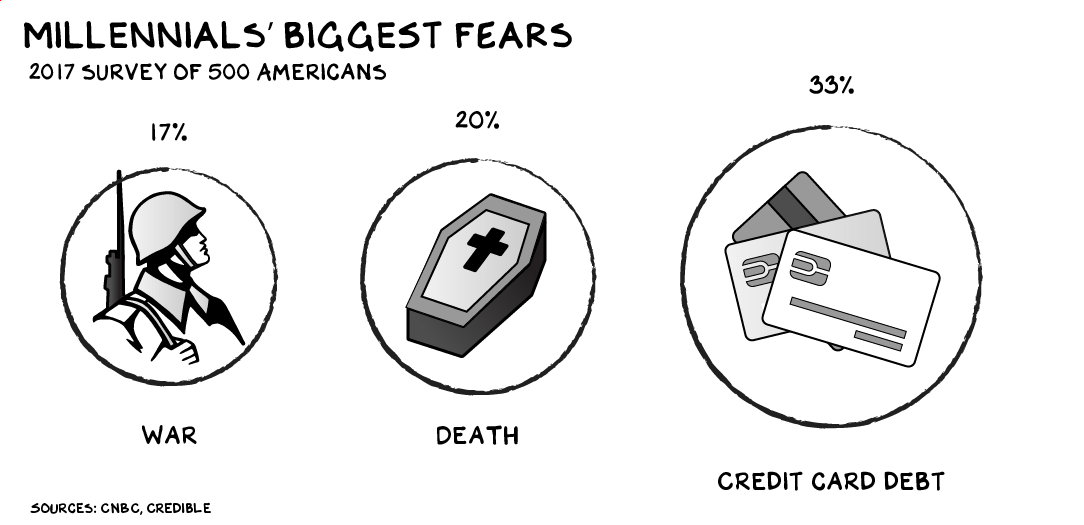

He’s not wrong. As Klarna reported in an investor factsheet, 1 in 3 millennials’ biggest fear is credit card debt. That’s more than name death or war. Deployment to Afghanistan is bad, but an unpaid balance on your Discover Card is (apparently) worse.

There’s one problem: Buy Now Pay Later is (wait for it) credit.

Hiding in Plain Sight

By most measures, BNPL services aren’t even good credit offerings. With a traditional credit card, you pay nothing up front, then you’ve got, on average, five weeks to pay without incurring any fees or interest. Closer to two months if you manage your billing cycles carefully. Carrying a balance will cost you, though, 1%-2% in interest per month. Miss a payment, and you get a late fee, about $30 — on which you’ll also pay interest.

In the short term at least, BNPL terms are worse. Take Afterpay. When you buy your new jeans, you have to come up with 25% of the money at purchase, then the lender gives you six weeks to pay off the remainder, in three installments. Miss an installment, and Afterpay hits you with a late fee. Continue in arrears, and the late fees increase, up to a cap of 25% of the purchase price. Also, you need a debit or credit card to make payments to Afterpay. Other providers have different fee and interest structures, but the basic model is the same. It’s credit.

BNPL companies market these limitations as features, not bugs. Because credit cards let you roll over your balance for a low monthly interest charge, you can rack up an insurmountable debt, which is harder to do with BNPL. Afterpay further limits customers’ risk by cutting them off once they start missing payments. It’s credit with training wheels, really. But it’s still credit.

BNPL marketing is Don Draper in Allbirds and a Patagonia vest, messaging for a modern age that generates irrational margins for the brand. Afterpay promotes that it charges “no interest!” However, miss one installment and you’re likely paying more, whether it’s called interest or a late fee. Afterpay competitor Affirm advertises the opposite: “Simple interest and no fees.” It then reiterates the message: “We don’t charge fees of any kind — not even late fees.” Bottom line, they’re all charging you the same thing: money.

Money Machine

So what’s the harm? Why not have a credit card with training wheels to ease young people into their journey toward a lifetime of debt? Especially as some of the costs are borne by the retailer in exchange for the consumer buying more sooner. Might Buy Now Pay Later even be training consumers to develop better purchase habits?

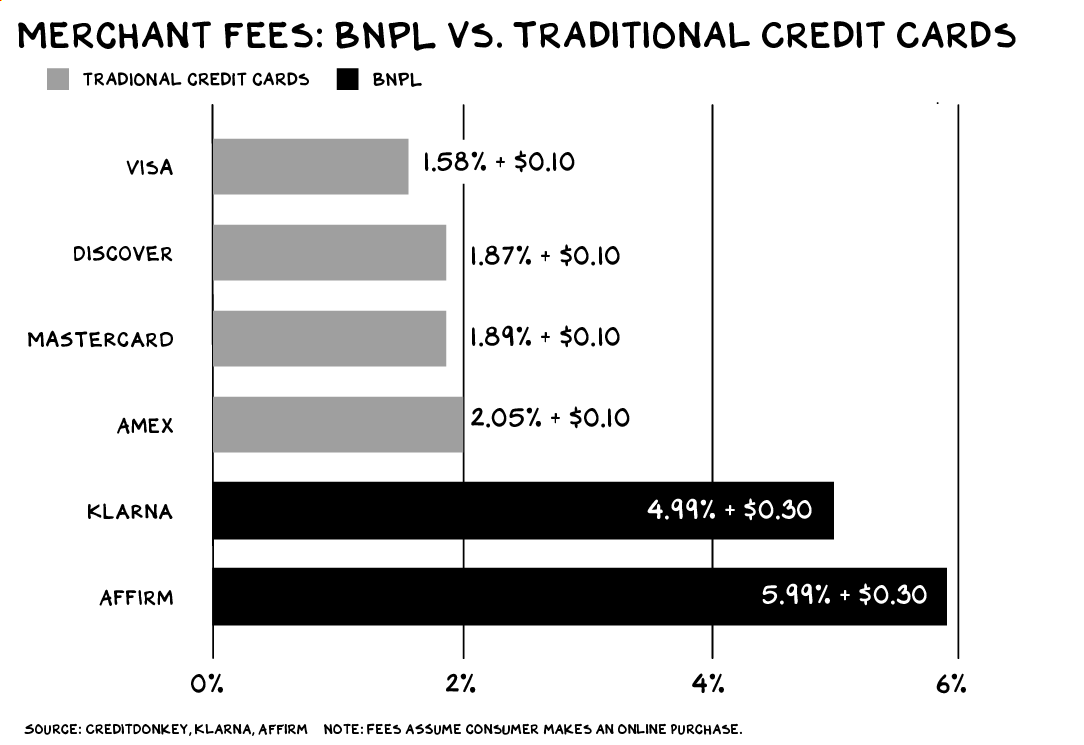

Here’s a good reason to be skeptical. (Let’s be honest, I’m skeptical about pretty much everything.) Pretending to be debit when you’re credit is an awesome business. BNPL firms take a larger cut of merchant sales than any other credit card company. Even AmEx — which charges merchants high interchange fees because its wealthy clientele are likely to spend more — gets a smaller share than Klarna, Affirm, and the like. Why would retailers do this? Because this technology/branding/sleight of hand convinces people to spend more than they would otherwise … full stop.

The business model is predicated on this fact: BNPL customers spend more money. Klarna boosts the average consumer basket size by 45%. Affirm increases it by 85%. Afterpay reports a 17% larger shopping cart, as well as a 12% uplift in overall sales. This is the psychological masterpiece at the heart of BNPL’s success: While fear of debt draws consumers toward Buy Now Pay Later, the model inspires them to spend more.

BNPL marketing teams are careful not to emphasize this with consumers. But on the merchant side, it’s the main event. More and more retailers are installing BNPL offerings at checkout, because they know consumers will load up their shopping carts. As a result, Afterpay’s merchant network has grown 500%+ since 2018.

Vulnerable

Buy Now Pay Later firms are quick to tell you that this is where they make most of their money — off merchants, not millennials. That’s true. But the business model only works by capitalizing on the instinct for immediate gratification. And younger neurons are more vulnerable to this marketing than older ones. The prefrontal cortex — the part of the brain linked to dopamine control and release — only finishes maturing at around 25 years old. As a result, younger people are far more likely to engage in risky behavior in search of instant gratification and quick dopa-hits. This is what makes trades on Robinhood, likes on Instagram, and purchases on BNPL so much more rewarding to young adults: They’re engineered to satisfy their neurocognitive architecture.

The problem is the companies are putting these people in debt. (Something I do every day: “NYU Professor of Marketing”. But I digress.) Australia’s financial regulator found 15% of BNPL users had to take out another loan to make their payments, and 1 in 5 had to cut down spending on essentials to make them. In 2019, Australian BNPL providers raked in $43 million in revenue from late fees, up 38% from the previous year. At a major U.K. bank, 10% of customers making BNPL payments overdrew their checking accounts in the same month. The authors of one study dubbed BNPL users “Generation Debt Trap.”

Scott Galloway’s posts often make me think. This one definitely spurred thought.