“We came from Caladan—a paradise world for our form of life. There existed no need on Caladan to build a physical paradise or a paradise of the mind—we could see the actuality all around us. And the price we paid was the price men have always paid for achieving a paradise in this life—we went soft, we lost our edge.” | Dune by Frank Herbert

Once we taste privilege, “stay hungry, stay foolish” is easier said than done.

Disneynature released another great documentary about a family of tigers recently. We’ve enjoyed all their previous ones (special shout-out to the polar bear and Dolphin reef) and this was another masterclass in storytelling.

This story was about a tigress raising four kids in the forests of Central India. In the middle of the story, she loses two of her kids as she’s forced to be away from them for a few days. After frenzied searching, she sees vultures around tiger carcasses and assumes both to be dead.

While one of them did sadly die, the other, a tigress named Charm, survived the ordeal against the odds. The scene where she reunites with her family after the ordeal is heartwarming. Her joy and relief is palpable.

Until that ordeal, Charm was consistently the most careful and shy of the four siblings. However, she comes back transformed. The ordeal helped her develop character and get in touch with her resilience. When it was time for the kids to finally leave their mother, it is Charm who leads the way.

That’s the paradox bad experiences present. We’d never want to wish them on us or anyone we care about. But, on the flip side, they help us build resilience and character.

So, if we aren’t going through an ordeal, there’s a lot to be grateful for.

A few years ago, a wise colleague shared some sage career advice – “Don’t swing at every pitch.” Career choices have high switching costs and it helps to be discerning as we consider new opportunities.

However, this post isn’t about career choices.

I’ve been thinking about this advice in the context of work more broadly. In any given day or week, we might experience many triggers for frustration or annoyance. It could be indirect – an inaccurate insight being shared widely, a document with false assertions, or some other perceived injustice. It could also be direct – someone saying something unfair directly to us or about us.

If we work with enough humans or in large enough organizations, we’re likely to experience such triggers often. And it can be easy to get caught in a reactionary cycle.

I think of these triggers as pitches. We can swing at every one of them that comes our way – but we’ll tire ourselves out needlessly.

Every action doesn’t deserve an equal and opposite reaction. Few are worth the effort.

It pays to focus on the signal while ignoring the noise.

For most folks who decide to do so, buying a home is the among the most significant transactions they’ll make in their lifetime. As a result, it is a high-pressure transaction. Ahead of our search, we emailed a few friends who’d bought recently and asked them to share their advice. Over time, I’ve since dispensed said advice and refined my own. My current synthesis has 3 notes –

(1) Picking a budget is a criticaldecision – pick an amount of debt that doesn’t add too much pressure for too long: Unless you’re wealthy and have no need for financial advice, your mortgage will change how you approach the next few years of your life. Some change is par for the course. But if it constrains your freedom and optionality (e.g., by making you feel too tied to your current job) for too long, it can become problematic quickly.

Buying a home is a lovely thing. It helps to budget for it in a way that it doesn’t become the only lovely thing you can afford in your life for the foreseeable future.

(2) There are things that can be easily changed and things that can’t – pay attention to the latter: There’s a lot about the look-and-feel of the house that can be changed. Floors can be changed, rooms can be redone, and bathrooms can be remodeled. These are problems that can solved with money.

On the flip side, problems that aren’t easily solved with money are structural issues in the home (especially those involving mold), a problematic homeowner’s association, and those involving the neighborhood – e.g., bad neighborhood schools or crime. Buying an okay home in a great neighborhood typically trumps buying a great home in a bad neighborhood.

(3) There is no such thing as a perfect home – instead, there is a great choice out there for you at this timewith trade-offsyou’re happy to live with. Assuming money is a constraint (see (1)), the home-buying decision is an exercise in trade-offs. You can’t have everything – you’ll have to just choose among the inventory available at any given time anyway.

If you want location, you’ll have to give up space. If you want space, you’ll have to do the work to maintain it. If you want a lot of space at a great price, you’ll likely have to make peace with a commute. Or if you decide you don’t want to deal with these trade-offs, you’ll have to wait a while before you buy – that’s a trade-off too.

There’s no right or wrong answer here. The reason to buy a home is because we believe it will increase the joy in our lives. Joy doesn’t come without pain. We just get to choose the kind of pain we want to deal with.

We met a teenager in our neighborhood the other day. He’d come home for a quick paid side-project. We learnt that he was saving up ahead of college in the fall.

He shared that this was his second attempt at college. He went to a college in Montana last year and he experienced so much hate because he was from California. So much so that he decided to not go back after the first semester.

We wished him all the best with this second attempt.

While it is hard to know the full picture in stories like this, it got me reflecting about how we’re so wired to think in terms of “us” and “them.” And that’s without any notion of typical dividers like skin color or religion or political affiliation (which just amplify differences). He was a gentle Caucasian kid who likely looked no different than those who drove him away.

I remember thinking about this when I was in college as well. I was part of a cohort of 100 Indian kids out of 1000 “international students” out of an incoming cohort of 6000. You’d think the relatively small group of Indian kids would stick together. But, no.. 100 is plenty for all sorts of “others.” The primary excuses for division among us was language.

If it wasn’t that, it was something else. There’s always something.

We are social creatures and it is in our nature to seek affiliation. Being tribal and exclusionary is the dark side of that propensity.

It is a reminder of just how hard it is to be inclusive and open to differences.

We won’t always succeed but it is important to try – both for the well-being of those “others” and ourselves. Our ability to make peace with those differences outside of us is generally indicative of the peace within.

“It’s so hard to forget pain, but it’s even harder to remember sweetness. We have no scar to show for happiness. We learn so little from peace.” | Chuck Palahniuk

I came across a summary of Robert Greene’s 48 Laws of Power in a newsletter recently. Here are 3 ideas that I found myself reflecting on –

On anger — Don’t express it directly. Channel it into your work and productivity. Anger expressed directly often leads to irrational behavior and words you later regret.

On trust — Never completely trust people right away, no matter how nice or competent they seem. Look closely for subtle cracks and inconsistencies in their character before investing time and energy into the relationship.

On criticism — Don’t take criticism personally. Look at it from the outside, as valuable feedback that can help you improve. The more open you are to criticism, the more you will learn.

I read the book more than a decade ago. I was early in my career and remember finding the book a bit dark. For a few days, I kept an eye out for power games everywhere. But, Robert Greene is a talented writer. And the book had insights and well researched wisdom on dealing with human problems.

As I reflect on the difference in my naivete and idealism today relative to that period, I think more of it would have resonated if I read it now. :-)

Every time I think Morgan Housel can’t possibly raise the bar with a post, he does. This is his post – “How I Think About Debt” in full.

Japan has 140 businesses that are at least 500 years old. A few claim to have been operating continuously for more than 1,000 years.

It’s astounding to think what these businesses have endured – dozens of wars, emperors, catastrophic earthquakes, tsunamis, depressions, on and on, endlessly. And yet they keep selling, generation after generation.

These ultra-durable businesses are called “shinise,” and studies of them show they tend to share a common characteristic: they hold tons of cash, and no debt. That’s part of how they endure centuries of constant calamities.

I love the quote from author Kent Nerburn that, “Debt defines your future, and when your future is defined, hope begins to die.”

Not only does hope begin to die, but the number of outcomes you can endure does, too.

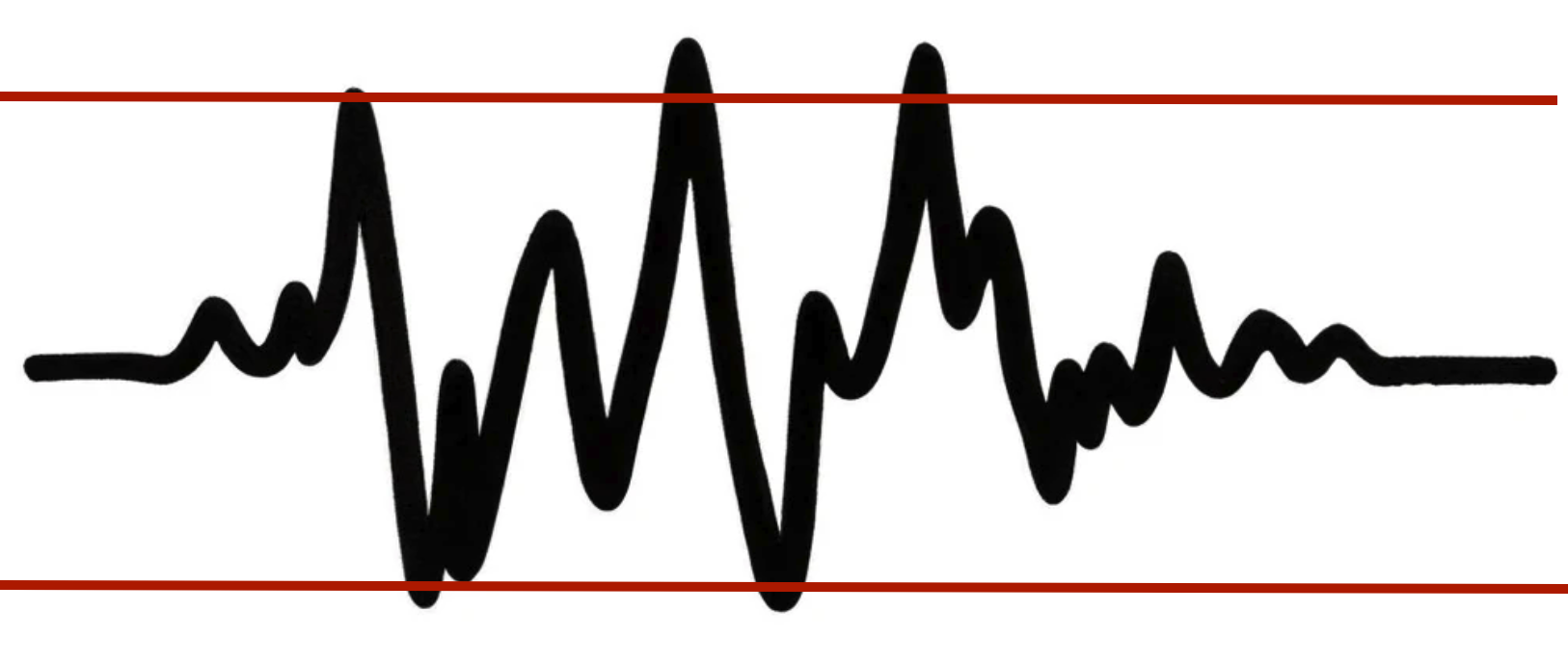

Let’s say this represents volatility over your life. Not just market volatility, but life world and life volatility: recessions, wars, divorces, illness, moves, floods, changes of heart, etc.

With no debt, the number of volatile events you can withstand throughout life might fall within a range that looks like this:

A few extreme events might do you in, but you’re pretty durable.

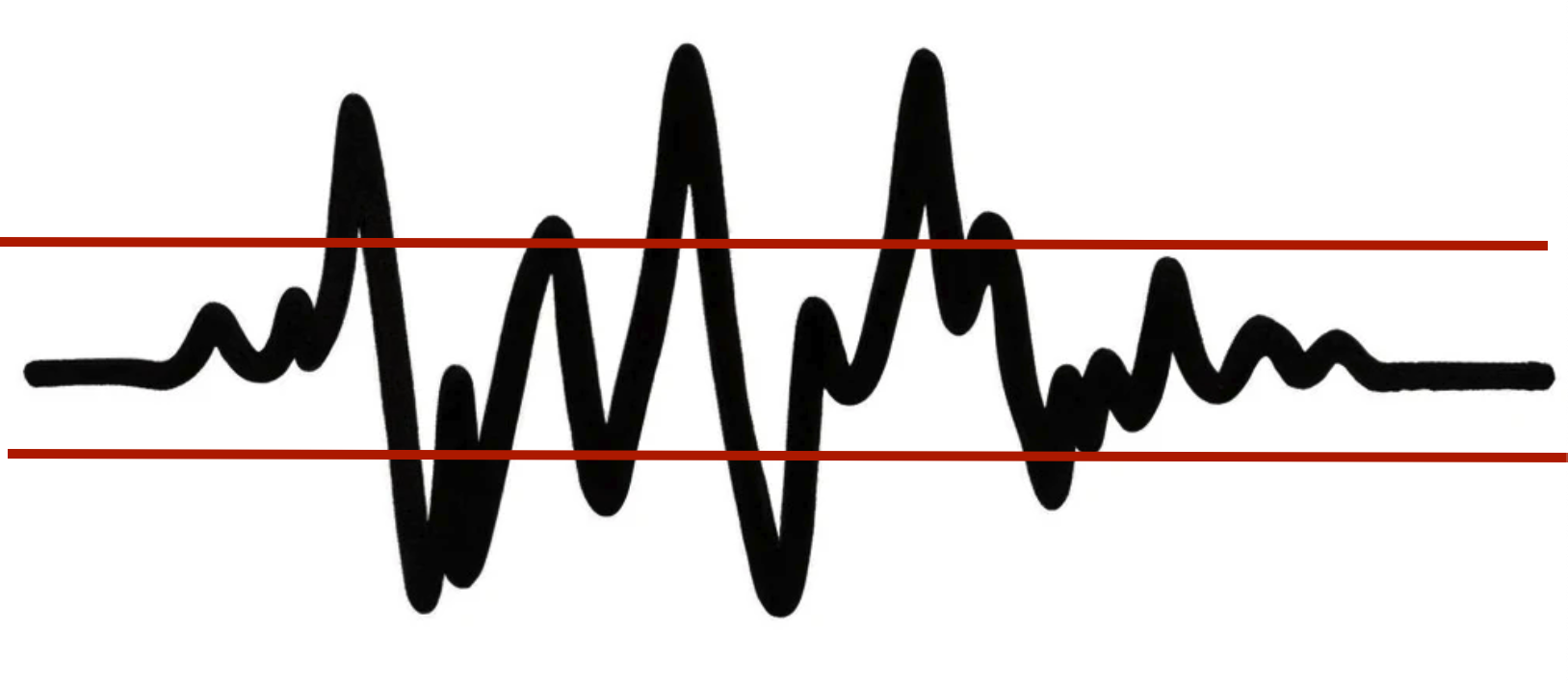

With more debt, the range of what you can endure shrinks:

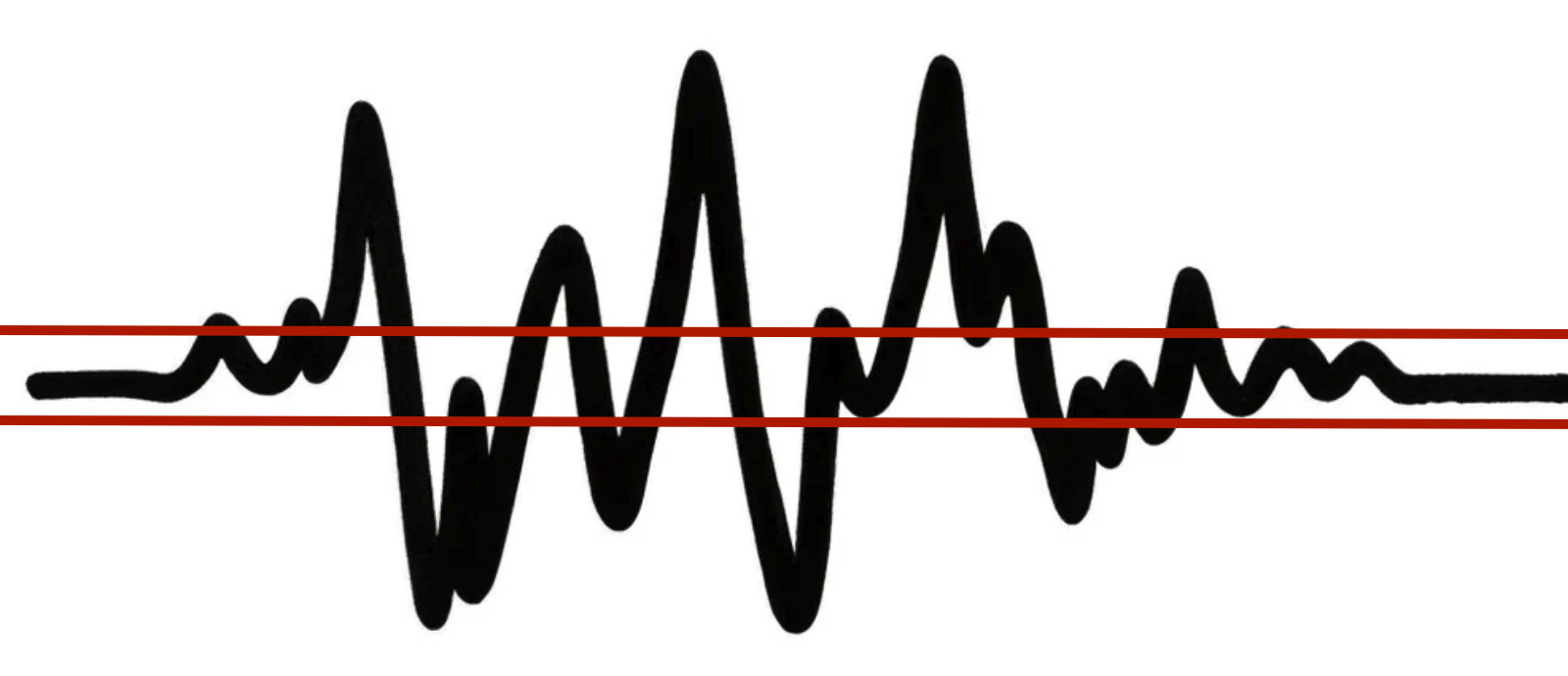

And with tons of debt, it tightens even more:

I think this is the most practical way to think about debt: As debt increases, you narrow the range of outcomes you can endure in life.

That’s so simple. But it’s different from how debt is typically viewed, which is a tool to pull forward demand and leverage assets, where the only downside is the cost of capital (the interest rate).

Two things are important when you view debt as a narrowing of endurable outcomes.

One is you start to ponder how common volatility is.

I hope to be around for another 50 years. What are the odds that during those 50 years I will experience one or more of the following: Wars, recessions, terrorist attacks, pandemics, bad political decisions, family emergencies, unforeseen health crises, career transitions, wayward children, and other mishaps?

One-hundred percent. The odds are 100%.

When you think of it like that, you take debt’s narrowing of survivable outcomes seriously.

The other is you think about the kinds of volatile events that could do you in.

Financial volatility is an obvious one – you find yourself unable to make your debt payments. But there’s also psychological volatility, where for whatever reason you can’t mentally endure your job any longer. There’s family volatility, which can be anything from divorce to caring for a relative. There’s child volatility, which could fill a book. Health volatility, political volatility, on and on. The world’s a wild place.

I’m not an anti-debt zealot. There’s a time and place, and used responsibly it’s a wonderful tool.

But once you view debt as narrowing what you can endure in a volatile world, you start to see it as a constraint on the asset that matters most: having options and flexibility.

“I will face my fear. I will permit it to pass over me and through me. And when it has gone past I will turn the inner eye to see its path. Where the fear has gone there will be nothing. Only I will remain.” ― Frank Herbert, Dune

We don’t make good decisions when we react to fear. It is an emotion that often gets the better of us.

This note is such a beautiful way to think about fear. It treats it like a strong gush of wind while conveying agency (“I will permit it to pass”) and permanency (“Only I will remain”).

I was a renter for over a decade and experienced many renter stories second-hand thanks to tales from friends. I mentally classified homeowners and apartment management companies in two categories – the short-cut takers and the long-term investors.

The difference between the two was simple. When faced with a choice, the former took a shortcut – typically the cheapest available quick fix. The latter, on the other hand, did their best to make the right long-term choice.

Both did so consistently. And it showed in the homes they rented out and in the renter experience. The former nickle-and-dimed renters and the latter were a pleasure to work with. They weren’t a pleasure to work with because they expected a yelp review. That’s just who they were.

This idea extends well outside the realm of renting homes. It applies to relationships, to building products, and to decisions we make in our lives.

Quick short-term fixes are a drug that are easy to get addicted to. They also work like drugs – ruining the long-term health of the people involved.

The best thing we can do for ourselves is to surround ourselves with people who unerringly make the right long-term call.